Joachim Kuczynski, 14 November 2025

This article shows how to derive the WACC (weighted average cost of capital) of a project from the WACC of a company (or asset portfolio in general). Further on company and portfolio have the same meaning. Let us assume a company or portfolio with  projects. The relative share of project

projects. The relative share of project  in the portfolio is

in the portfolio is  . The WACC of project is

. The WACC of project is  . The cost of capital of the portfolio,

. The cost of capital of the portfolio,  , is given by:

, is given by:

(1)

That means that the WACC of a portfolio is the weighted average of the components’ WACC.

Let us have a look at the variance of the portfolio WACC:

(2)

The covariance is bilinear, we get:

(3)

The correlation of an asset’s WACC with the portfolio’s WACC is defined by:

(4)

and

and  are the standard deviations of and . Substituting covariance by correlation we get:

are the standard deviations of and . Substituting covariance by correlation we get:

(5)

Dividing by the standard deviation  leads us to the standard deviation of the portfolio:

leads us to the standard deviation of the portfolio:

(6)

That means that the incremental risk contribution of each project to the risk of the portfolio is  and not just the weighted sum of its projects’ risks. Hence we can e.g. reduce the WACC of the portfolio by adding a project with negative correlation to the portfolio.\

and not just the weighted sum of its projects’ risks. Hence we can e.g. reduce the WACC of the portfolio by adding a project with negative correlation to the portfolio.\

Instead of including a new project to the portfolio the company can also increase the return of the portfolio by increasing the risk of the portfolio. This reward-to-volatility ratio of the tangential portfolio is given by the Sharpe Ratio:

(7)

is the expected value of and

is the expected value of and  is the after-tax debt interest rate. The company wants to invest in the new project, if the additional WACC of this project is lower than an investment in the existing portfolio with the same risk changes. Hence we obtain the requirement to invest in the new project:

is the after-tax debt interest rate. The company wants to invest in the new project, if the additional WACC of this project is lower than an investment in the existing portfolio with the same risk changes. Hence we obtain the requirement to invest in the new project:

(8)

With that we can define the sensitivity  of the new project to the existing portfolio:

of the new project to the existing portfolio:

(9)

Substituting with the requirement for the new investment becomes the well-known equation:

(10)

With that we can define a maximum annual WACC of the additional project. This is the maximum WACC at which a company would decide to invest in the project.

(11)

Let us assume that the new project and the company are correlated completely, which means  . In this case we get:

. In this case we get:

(12)

The quotient  is called relative risk factor of project . The risk premium of the company WACC is adapted by the quotient of the standard deviations of the project and the company. The higher the risk of the project the higher the required WACC of the project to become a new part of the company portfolio. If the risk of the project and the risk of the company are the same, the WACC of the project and the company are the same, too. The standard deviation can be generated by Monte Carlo Simulation or approximated by best/worst case scenarios. Another approach is to estimate the standard deviations by management. Instead of comparing the project to the whole company portfolio we can also compare it to a benchmark project. This benckmark project is considered to be representative for the company.

is called relative risk factor of project . The risk premium of the company WACC is adapted by the quotient of the standard deviations of the project and the company. The higher the risk of the project the higher the required WACC of the project to become a new part of the company portfolio. If the risk of the project and the risk of the company are the same, the WACC of the project and the company are the same, too. The standard deviation can be generated by Monte Carlo Simulation or approximated by best/worst case scenarios. Another approach is to estimate the standard deviations by management. Instead of comparing the project to the whole company portfolio we can also compare it to a benchmark project. This benckmark project is considered to be representative for the company.

and equity return rates

and equity return rates  .

.  data pairs.

data pairs.  and

and  are the arithmetic mean values of

are the arithmetic mean values of  .

.

of the linear regression function

of the linear regression function

and

and

is given by:

is given by:

) in the Capital Asset Pricing Model (CAPM). That means that

) in the Capital Asset Pricing Model (CAPM). That means that

… net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

… net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

be the incremental tax rate. We assume that we get full tax shield of

be the incremental tax rate. We assume that we get full tax shield of  . Taxes

. Taxes  are paid on EBIT, that means

are paid on EBIT, that means  .

.  =equity+debt is the asset or enterprise value and d is the debt ratio,

=equity+debt is the asset or enterprise value and d is the debt ratio,  . Substituting that in the previous expression we obtain:

. Substituting that in the previous expression we obtain:

,

,  ,

,  . Variable expenses should have the same correlation to market development as sales, that gives

. Variable expenses should have the same correlation to market development as sales, that gives  . We obtain:

. We obtain:

leads to:

leads to:

with its bilinearity of covariance and get:

with its bilinearity of covariance and get:

as function of

as function of  :

:

.

.

ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that

ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that  by a given market return rate

by a given market return rate

:

:

,

,  ,

,  ,

,  and

and  . Now we take the parameters of the investment, to which we want to adjusted

. Now we take the parameters of the investment, to which we want to adjusted  . With the

. With the

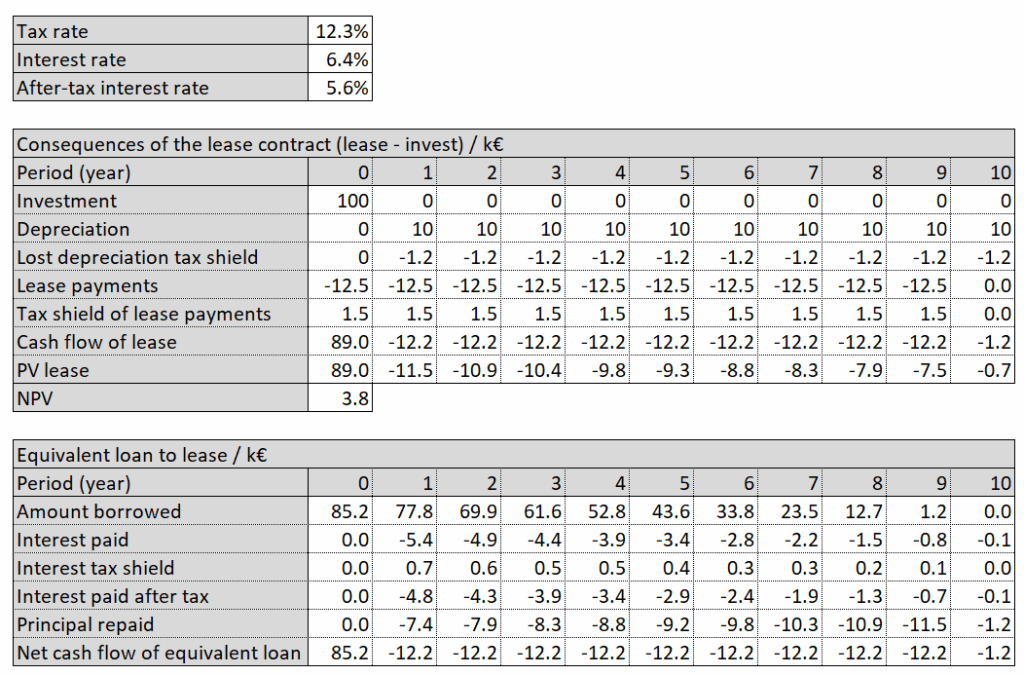

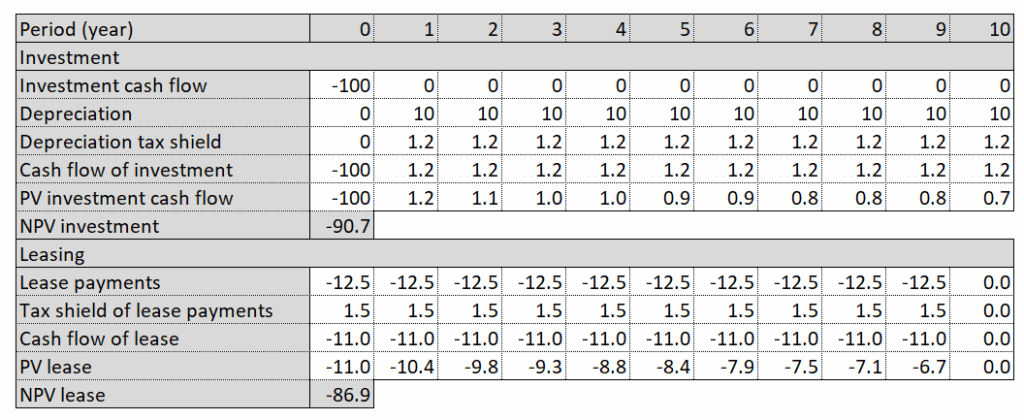

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate  , a tax rate

, a tax rate  we get the net value of lease

we get the net value of lease  :

:![\[V_l=I-\sum_{t=0}^{n}\frac{C_t}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2a7aa6733405981af5a4daba9e405359_l3.png "Rendered by QuickLaTeX.com")

means that leasing is better than doing the investment,

means that leasing is better than doing the investment,  indicates that leasing is worse than investing.

indicates that leasing is worse than investing.

be the investment scenario cash flow and

be the investment scenario cash flow and  be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:

be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:![\[\sum_{t=0}^{n}\frac{\left( C_{i,t} - C_{l,t} \right)}{\left( 1+r_d \left(1-r_t \right)\right)^t}=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bbdbe0b0f75b2a0f8bed462292847df8_l3.png "Rendered by QuickLaTeX.com")

![\[=\sum_{t=0}^{n}\frac{ C_{i,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}-\sum_{t=0}^{n}\frac{C_{l,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c1d6f85415bf645b3bede9acb1b6f5c1_l3.png "Rendered by QuickLaTeX.com")