Joachim Kuczynski, 24 October 2023

Introduction

In this article I want to derive the explicit relationship between an option value and the probability of occurrence of its event states in the binomial model of Cox, Ross and Rubinstein. In many cases I read that the risk neutral probabilities and therefore the option value do not depend on the probabilities of the real state values. But the options values depend on them implicitly. That is what I will derive in this post.

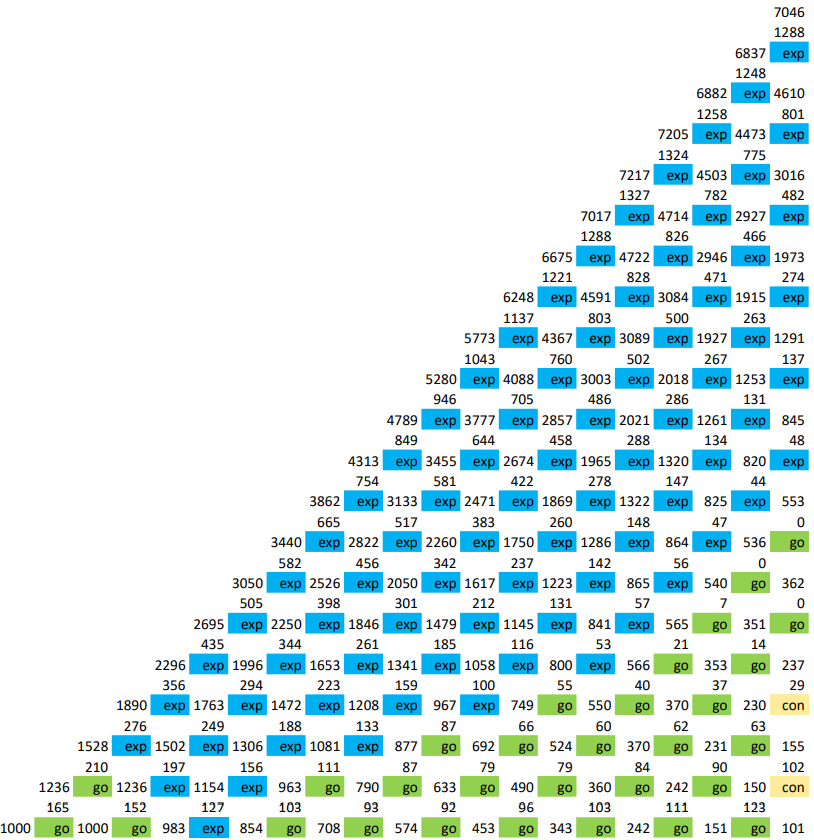

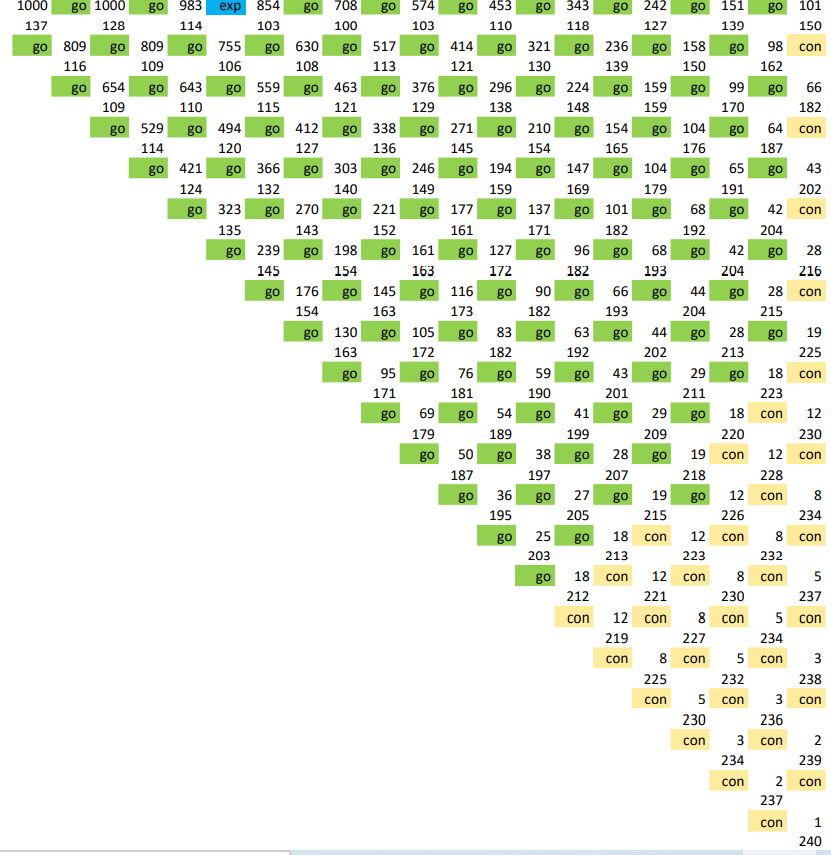

Binomial Model by Cox, Ross and Rubinstein

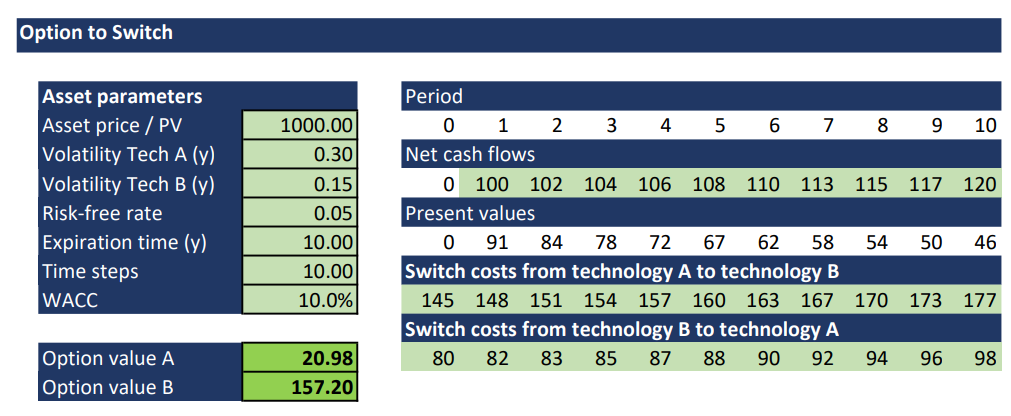

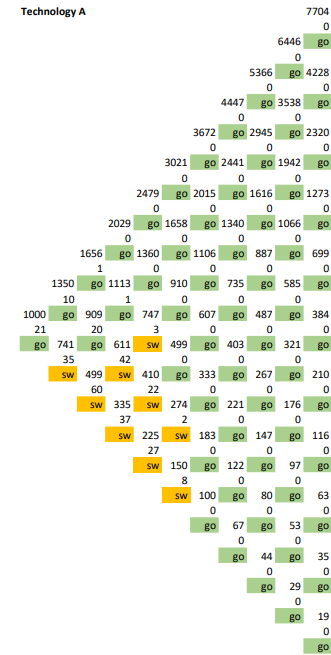

Options can be valued with the binomial model from Ross, Cox and Rubinstein. The value  of an option at time

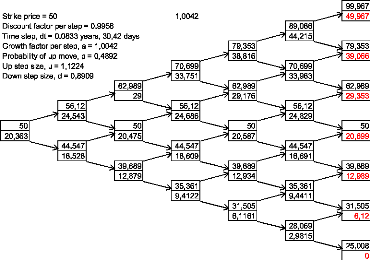

of an option at time  is given by:

is given by:

![\[C_0=\frac{\alpha C_{u,t_1}+(1-\alpha )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d245e3e501c03334a52b0327fc44aea3_l3.png "Rendered by QuickLaTeX.com")

and

and  are the option values of the up and down development at time

are the option values of the up and down development at time  .

.  is the risk free rate and T is the time between and

is the risk free rate and T is the time between and  ,

,  .

.  is the risk neutral probability of the up movement in ,

is the risk neutral probability of the up movement in ,  is the risk neutral probability of the down movement in . The binomial model provides the following relationship:

is the risk neutral probability of the down movement in . The binomial model provides the following relationship:

![\[\alpha=\frac{(1+r)^T-d}{u-d}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-53e84d5ecdafd962f48030489a62864d_l3.png "Rendered by QuickLaTeX.com")

Including provides this expression for

![\[C_0=\frac{\frac{(1+r)^T-d}{u-d} C_{u,t_1}+(1-\frac{(1+r)^T-d}{u-d} )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-4585ecf3307b3ea36a992a134bd156a8_l3.png "Rendered by QuickLaTeX.com")

Hence we obtain:

![\[C_0=\frac{( (1+r)^T-d ) C_{u,t_1}+(u-(1+r)^T )C_{d,t_1}}{(1+r)^T (u-d)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e41bd7434143afaf1fc36677db98383c_l3.png "Rendered by QuickLaTeX.com")

and

and  are defined as ratio of up and down movement in relation to the expected value in ,

are defined as ratio of up and down movement in relation to the expected value in ,  :

:

![\[u= \frac{EV(S_{t_0})}{S_{u,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d9deab9057d9c6d1f3a1ba8f0e6ce779_l3.png "Rendered by QuickLaTeX.com")

![\[d= \frac{EV(S_{t_0})}{S_{d,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-875c14eb30bf1a7d78b5173c9c6dfadf_l3.png "Rendered by QuickLaTeX.com")

Up to now the probabilities of up state  and down state

and down state  have not occured. Many times that leads to the argument that these probabilities do not influence the option value. But that is not true. The expected value of the state

have not occured. Many times that leads to the argument that these probabilities do not influence the option value. But that is not true. The expected value of the state  and therefore

and therefore  depends on the probabilities. The expected value of the event state in is the discounted value of event state in . With

depends on the probabilities. The expected value of the event state in is the discounted value of event state in . With  as yearly constant discount rate we get:

as yearly constant discount rate we get:

![\[EV(S_{t_0})=\frac{EV(S_{t_1})}{(1+D)^T}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{(1+D)^T}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1bde57d477d9f69bdf954feb24df97ba_l3.png "Rendered by QuickLaTeX.com")

For and we get the following:

![\[u=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{u,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ba3a6fc511e4ae945efcc80c544226d2_l3.png "Rendered by QuickLaTeX.com")

![\[d=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-df6488617bbde3eaabec1cf22b39708f_l3.png "Rendered by QuickLaTeX.com")

As final result we obtain:

![\[C_0=\frac{( (1+r)^T-\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}) C_{u,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}+\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0769b16c961ea4a991747ee6dec7ad23_l3.png "Rendered by QuickLaTeX.com")

![\[+\frac{(\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-(1+r)^T )C_{d,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5b78a3049855170fe758d7f83b5e5355_l3.png "Rendered by QuickLaTeX.com")

This is the basic relationship between the value of an option at a time and explicit problem specific variables.

Conclusion

We realize that the option value expicitely depends on the probability  of the up state

of the up state  , and

, and  of the down state

of the down state  respectively. That is what we wanted to prove. The argument that this dependency does not exist, does not take into account that the value of state

respectively. That is what we wanted to prove. The argument that this dependency does not exist, does not take into account that the value of state  depends on the state probabilities in . Hence there is no disappearance mystery of real life or real states probabilities in options valuation. q.e.d.

depends on the state probabilities in . Hence there is no disappearance mystery of real life or real states probabilities in options valuation. q.e.d.

, initial state

, initial state  , an up-state of

, an up-state of  in

in  and a down state of

and a down state of  in

in  . The probability of an up movement is assumed to be

. The probability of an up movement is assumed to be  . The expected value after the first time step

. The expected value after the first time step  and has to be the same as the expected value of the two binomial states in

and has to be the same as the expected value of the two binomial states in ![\[p S_0 u + (1-p) S_0 d=e^{\mu \Delta t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-798ff5d7793935afadeda0d98e8a508e_l3.png "Rendered by QuickLaTeX.com")

be the expected value of a random variable

be the expected value of a random variable  . Then the variance

. Then the variance  of

of ![var(X)=E(X^2)-[E(X)]^2.](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ef9c2e3a7bebc53bf55716b26c457dd1_l3.png "Rendered by QuickLaTeX.com") With that the variance of the two states of the binomial tree in

With that the variance of the two states of the binomial tree in ![\[pS_0^2 u^2+(1-p) S_0^2 d^2-(puS_0+(1-p)dS_0 )^2 \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-b40cce08cb257a30a2533d6c33aebde4_l3.png "Rendered by QuickLaTeX.com")

be the expected annual volatility of the process.

be the expected annual volatility of the process.  of the annual relative returns:

of the annual relative returns:![\[\frac{ \Delta S}{S} \thickapprox \Phi ( \mu \Delta t, \sigma \sqrt{\Delta t})\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-33253f0f61f87179b215093cf3718139_l3.png "Rendered by QuickLaTeX.com")

![\[var(S)=S^2 \sigma ^2 \Delta t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6930a74f740ca2c64046a48a32f67312_l3.png "Rendered by QuickLaTeX.com")

![\[p u^2 + (1-p) d^2 - ( p u+ (1-p) d)^2 = \sigma ^2 \Delta t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-df21a7ea2b5d2532cd32e35b5bf1fb78_l3.png "Rendered by QuickLaTeX.com")

and higher powers of

and higher powers of ![\[u=e^ {( \sigma \sqrt {\Delta t})}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-04e26ccfd9eae55aa492ba70387207c3_l3.png "Rendered by QuickLaTeX.com")

![\[d=e^ {( - \sigma \sqrt {\Delta t})}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-609fa294bf4028d8e72d7fd68fe830a1_l3.png "Rendered by QuickLaTeX.com")

, when

, when

be the value of the underlying asset in

be the value of the underlying asset in  , occurs with probability

, occurs with probability  in

in  ,

,  ,

,  ,

, in

in  in the upper state

in the upper state  in the lower state

in the lower state  shares of twin security

shares of twin security  at the risk-free rate

at the risk-free rate  and

and  .

. we get:

we get:![\[n=\frac{E^+-E^-}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0f1b9697c29529cdc9d6fb23d9232485_l3.png "Rendered by QuickLaTeX.com")

![\[B=\frac{1}{1+r}\frac{{E^+S^--E}^-S^+}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ac35b5d4ad5fc53d32028c8dc64933fd_l3.png "Rendered by QuickLaTeX.com")

. With that we calculate the value of the option in

. With that we calculate the value of the option in ![\[E=\frac{\left(\frac{S\left(1+r\right)-S^-}{S^+-S^-}\right)E^++\left(1-\frac{S\left(1+r\right)-S^-}{S^+-S^-}\right)E^-}{1+r}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bccf07b0c1c2c9b722c78bf7bd5bfd44_l3.png "Rendered by QuickLaTeX.com")

to simplify the previous expression.

to simplify the previous expression.![\[p^\prime=\frac{S\left(1+r\right)-S^-}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a79fb856ce26df70c2d45b3cf96f8461_l3.png "Rendered by QuickLaTeX.com")

![\[E=\frac{p\prime E^++\left(1-p\prime\right)E^-}{1+r}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-05a980182c7265f624712db1703bf91c_l3.png "Rendered by QuickLaTeX.com")

for

for