Joachim Kuczynski, 05 April 2025

In this post I want to explain how you can estimate the discount rate of contribution (or variable) cash flows using perpetuity.

From external data we get a discount rate of an asset with comparable risk portfolio and volatility. Next we have to adjust this discount rate for financial leverage and cash. If the investor’s portfolio is not diversified sufficiently we also have to adapt to this lack of diversification. As result we get an adjusted asset discount rate  .

.

Now we want to seperate the fixed cash flows from the asset cash flows and figure out the discount rate of variable cash flows  . Discount rate of fixed cash flows is

. Discount rate of fixed cash flows is  .

.

We consider all yearly cash flows to be constant in the future. The yearly variable cash flow is  and the yearly fixed cash flow is

and the yearly fixed cash flow is  . Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is

. Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is  . Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series.

. Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series.

Let us now have a look at the present values of the 3 cash flow types in the end of period 0.  is the present value of

is the present value of  discounted with .

discounted with .  is the present value of discounted with .

is the present value of discounted with .  is the present value of discounted with .

is the present value of discounted with .  is the present value of discounted with .

is the present value of discounted with .  is the present value of discounted with .

is the present value of discounted with .

We have convergent geometric series, hence we obtain:

![\[ V_a^a = \frac{C_a}{r_a}, V_f^a=\frac{C_f}{r_a}, V_f^f=\frac{C_f}{r_f},V_v^a=\frac{C_v}{r_a},V_v^v=\frac{C_v}{r_v} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a5e1ac4bc9c18e87411a96b62844a496_l3.png "Rendered by QuickLaTeX.com")

The present value of the asset  has to be the same when we discount all cash flows with the asset discount rate as when discounting the variable cash flows with and the fix cash flows with seperately:

has to be the same when we discount all cash flows with the asset discount rate as when discounting the variable cash flows with and the fix cash flows with seperately:

![\[ V_a^a=V_v^a+V_f^a=V_f^f+V_v^v \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-3206dc15e5c646023b4aa2e93680a8e8_l3.png "Rendered by QuickLaTeX.com")

After some transformations we obtain an expression for :

![\[ r_v=\frac{r_a}{1-\frac{C_f}{C_v}\left( \frac{r_a}{r_f}-1 \right)} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-95872d0a31aa511d42eef9c28dd1a8bb_l3.png "Rendered by QuickLaTeX.com")

I wrote the expression in this way to show that only depends on the ratio of  and not on their absolute values.

and not on their absolute values.

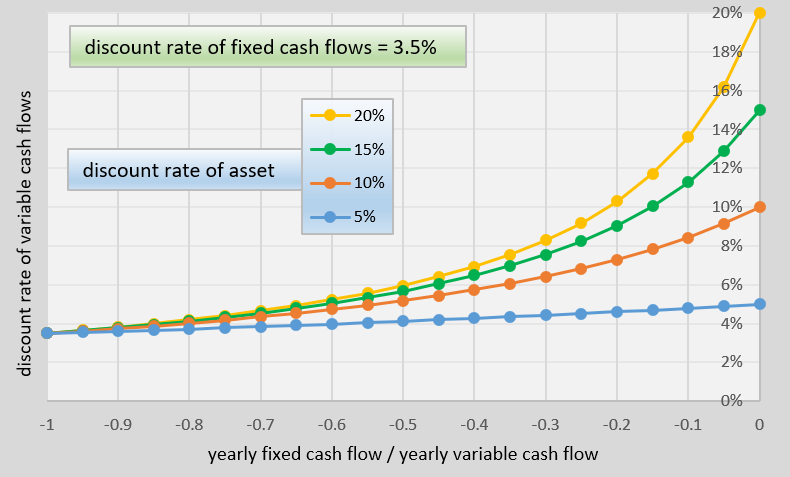

In the graph you can see the discount rate of variable cash flows as function of the ratio of yearly fixed to variable cash flows for different asset discount rates.

For  the

the  Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same.

Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same.

Ordinary projects with positive yearly asset cash flows have a fixed to variable cash flow ratios of approximately -0.1 to -0.4. The graph shows that the change of is highest in this range. Additionally you can see that adding fixed cash flows to a project decreases significantly.

These results can help you to seperate the discounting procedure in a DCF analysis into variable and fixed cash flow discounting. This may be important when the fixed and cash flows in your investment project occur in different time periods. For instance the investment cash flows in the beginning of the project and the variable cash flows (returns and variable costs) in later time periods.