Joachim Kuczynski, 01 November 2025

Net Income

With the abbreviations  … net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

… net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

(1)

Let  be the interest rate for debt and

be the interest rate for debt and  be the incremental tax rate. We assume that we get full tax shield of

be the incremental tax rate. We assume that we get full tax shield of  . Taxes

. Taxes  are paid on EBIT, that means

are paid on EBIT, that means  .

.  =equity+debt is the asset or enterprise value and d is the debt ratio,

=equity+debt is the asset or enterprise value and d is the debt ratio,  . Substituting that in the previous expression we obtain:

. Substituting that in the previous expression we obtain:

(2)

Summarizing the terms leads to:

(3)

Beta of a weighted sum is the weighted sum of the components’ betas, shown in the post “Portfolio Beta”. Thus we get an equation for the betas:

(4)

We assume that fix expenses (F), depreciation, amortization (A) and debt (D) have no correlation to the market return rate,  ,

,  ,

,  . Variable expenses should have the same correlation to market development as sales, that gives

. Variable expenses should have the same correlation to market development as sales, that gives  . We obtain:

. We obtain:

(5)

Substituting  leads to:

leads to:

(6)

Rearranging the terms shows:

(7)

Return on Equity

Return on equity measures relative equity increase. It is defined by:

(8)

With the substitution of we obtain:

(9)

We want to link the beta of ROE to the beta of net income. We take the definition of  with its bilinearity of covariance and get:

with its bilinearity of covariance and get:

(10)

Hence we get  as function of

as function of  :

:

(11)

(12)

This is the relationship of the ROE beta and the sales beta. It depends on several variables, but especially on fixed expenses  .

.

Releveraging Equity Return Rate and WACC

An equity investor wants to know which return rate market provides at the same risk (volatility) level as our investigated investment. The WACC after taxes of the appropriate market portfolio is given by:

(13)

I indicate all market portfolio parameters with a line on the top.  ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that can be approximated by a linear function of

ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that can be approximated by a linear function of  by a given market return rate

by a given market return rate  :

:

(14)

is the average equity of an market portfolio representing the investigated investment. It is based on an averaged financial and operating leverage of the market portfolio. If these parameters do not match capital and cost structure of the considered investment, you have to “releverage” .

Operating leverage: We have a look at the relationship of and  :

:

(15)

is provided by an official data collection in most cases. With the other data from the market portfolio we can calculate :

(16)

is the linear approximated change of sales because of a change in market return rate . does not depend on  ,

,  , ,

, ,  ,

,  and . is the same for all combinations of these parameters, that means

and . is the same for all combinations of these parameters, that means  . Now we take the parameters of the investment, to which we want to adjusted

. Now we take the parameters of the investment, to which we want to adjusted  . With the from the previous equation we obtain the adjusted :

. With the from the previous equation we obtain the adjusted :

(17)

With this we can calculate the new equity return rate  :

:

(18)

After the releveraging process we get the releveraged WACC with the appropriate :

(19)

. With that we obtain

. With that we obtain  .

. is:

is:![\[ r_v=r_f+\beta_v\left( r_m-r_f \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-3ee7dd71a1607b3846dc46be0f328058_l3.png "Rendered by QuickLaTeX.com")

![\[ r_a=r_f+\beta_a\left( r_m-r_f \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-da3fa7396c5319603d30e5fe815e0726_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v=r_a-r_f-\beta_a\left( r_m-r_f \right) + r_f+ \beta_v \left( r_m-r_f \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-63a0adfe7e092809b959ab3e12ab1ad8_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v=r_a- \left( r_m-r_f \right) \left( \beta_a -\beta_v \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7efc5a713f9f9b0200bdddf5a9b9fcb7_l3.png "Rendered by QuickLaTeX.com")

![\[ \beta_a=\beta_f\frac{-\left| V_f \right|}{V_a}+\beta_v\frac{V_v}{V_a}=\beta_v\frac{V_v}{V_a} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e5bf1006a9a0fce83b6285ba495466dd_l3.png "Rendered by QuickLaTeX.com")

![\[ \beta_a - \beta_v = \beta_a \left( 1-\frac{V_a}{V_v} \right) =\beta_a \frac{ \left| V_f \right| }{ \left| V_f \right| + V_a} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8b5c6ac60c6d868aabba62975ed83ee1_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v=r_a- \left( r_m-r_f \right) \beta_a \frac{ \left| V_f \right| }{ \left| V_f \right| + V_a} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-54e8e369fbe58654da69b8d7e1862eb5_l3.png "Rendered by QuickLaTeX.com")

by

by  leads to the final result:

leads to the final result:![\[ r_v= r_a- \left( r_a-r_f \right) \frac{ \left| V_f \right| }{ \left| V_f \right| + V_a}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-9f2ca73ccd5fd37c03e2e0248bc329a7_l3.png "Rendered by QuickLaTeX.com")

in the previous formula gives:

in the previous formula gives:![\[ r_v\left( V_f = 0 \right) = r_a \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e4f47b2c6bc8971d7a56ce97413b5de6_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v\left( V_a = 0 \right) = r_f \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2bb9db0ca6cadc95506696b31c1e081b_l3.png "Rendered by QuickLaTeX.com")

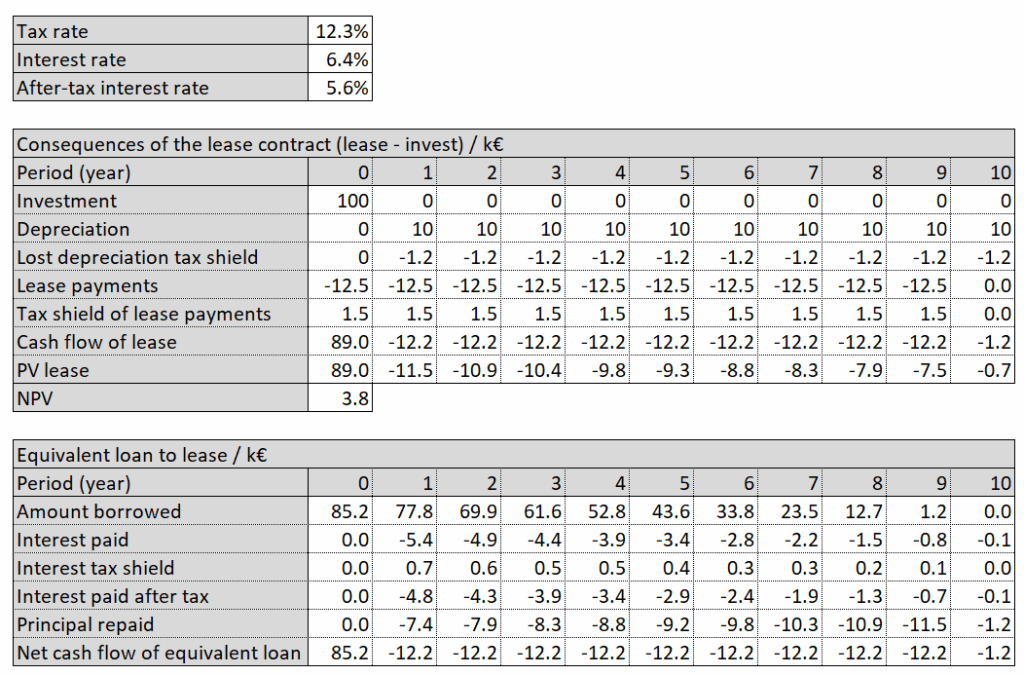

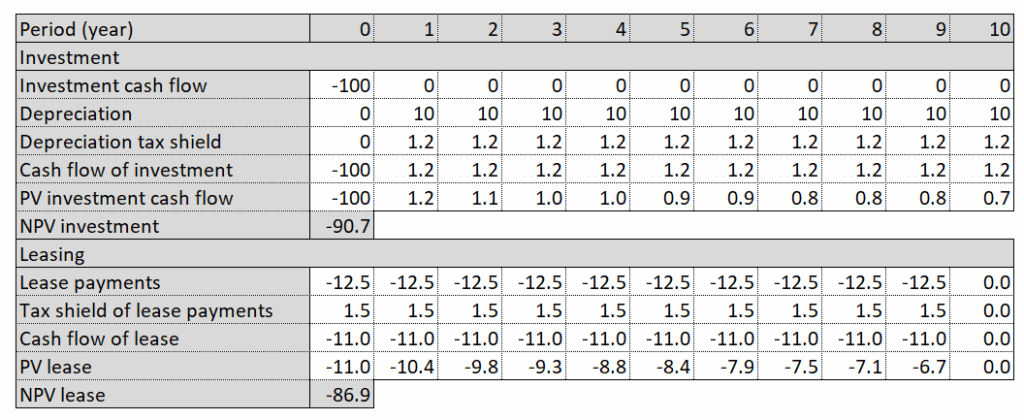

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate  , a tax rate

, a tax rate  we get the net value of lease

we get the net value of lease  :

:![\[V_l=I-\sum_{t=0}^{n}\frac{C_t}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2a7aa6733405981af5a4daba9e405359_l3.png "Rendered by QuickLaTeX.com")

means that leasing is better than doing the investment,

means that leasing is better than doing the investment,  indicates that leasing is worse than investing.

indicates that leasing is worse than investing.

be the investment scenario cash flow and

be the investment scenario cash flow and  be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:

be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:![\[\sum_{t=0}^{n}\frac{\left( C_{i,t} - C_{l,t} \right)}{\left( 1+r_d \left(1-r_t \right)\right)^t}=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bbdbe0b0f75b2a0f8bed462292847df8_l3.png "Rendered by QuickLaTeX.com")

![\[=\sum_{t=0}^{n}\frac{ C_{i,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}-\sum_{t=0}^{n}\frac{C_{l,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c1d6f85415bf645b3bede9acb1b6f5c1_l3.png "Rendered by QuickLaTeX.com")

is defined by:

is defined by:![\[\beta_p=\frac{cov(r_p,r_m)}{var(r_m)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d4ef4da8f1e8ab77a034e0b8da002c38_l3.png "Rendered by QuickLaTeX.com")

, is the weighted average of its components’ return rates:

, is the weighted average of its components’ return rates:![\[r_p=\sum_{i=1}^{n}\alpha_ir_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7a58dd9b270e96a227c4ced12ba0b223_l3.png "Rendered by QuickLaTeX.com")

stands for the relative value share of asset

stands for the relative value share of asset  in the portfolio. The covariance of two random variables is bilinear. Hence we get:

in the portfolio. The covariance of two random variables is bilinear. Hence we get:![\[cov(r_p, r_m)=cov(\sum_{i=1}^{n}\alpha_ir_i,r_m)=\sum_{i=1}^{n}\alpha_icov(r_p, r_m)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-10de1be8e0635eb826fdc60bf0e5ed6b_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_p=\frac{\sum_{i=1}^{n}\alpha_icov(r_p, r_m)}{var(r_m)}=\sum_{i=1}^{n}\alpha_i\beta_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6678a30fba9b392c30156bc1a214cd77_l3.png "Rendered by QuickLaTeX.com")

assets is the weighted average of its components, weighted by their relative value share in the portfolio.

assets is the weighted average of its components, weighted by their relative value share in the portfolio. .

. .

. and the yearly fixed cash flow is

and the yearly fixed cash flow is  . Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is

. Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is  . Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series.

. Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series. is the present value of

is the present value of  discounted with

discounted with  is the present value of

is the present value of  is the present value of

is the present value of  is the present value of

is the present value of  is the present value of

is the present value of ![\[ V_a^a = \frac{C_a}{r_a}, V_f^a=\frac{C_f}{r_a}, V_f^f=\frac{C_f}{r_f},V_v^a=\frac{C_v}{r_a},V_v^v=\frac{C_v}{r_v} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a5e1ac4bc9c18e87411a96b62844a496_l3.png "Rendered by QuickLaTeX.com")

has to be the same when we discount all cash flows with the asset discount rate

has to be the same when we discount all cash flows with the asset discount rate ![\[ V_a^a=V_v^a+V_f^a=V_f^f+V_v^v \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-3206dc15e5c646023b4aa2e93680a8e8_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v=\frac{r_a}{1-\frac{C_f}{C_v}\left( \frac{r_a}{r_f}-1 \right)} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-95872d0a31aa511d42eef9c28dd1a8bb_l3.png "Rendered by QuickLaTeX.com")

and not on their absolute values.

and not on their absolute values.

the

the  Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same.

Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same. from databases in literature or in the web. In my articles concerning

from databases in literature or in the web. In my articles concerning ![\[\beta^{ind}_{rev}=\beta ^{ind}_{asset} \left( 1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}} \right)^{-1}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cde5ba671ecc1b7b10012fd92a965c0e_l3.png "Rendered by QuickLaTeX.com")

. Hence we obtain:

. Hence we obtain:![\[\beta^{proj}_{rev}=\beta ^{ind}_{asset} \left( 1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}} \right)^{-1}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-353eccdb29a981373f6cdc4bca2ce048_l3.png "Rendered by QuickLaTeX.com")

![\[\beta^{proj}_{asset}=\beta ^{proj}_{rev} \left( 1-\frac{V^{proj}_{fix}}{V^{proj}_{asset}} \right)=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f653639fde45c24bb671287829805624_l3.png "Rendered by QuickLaTeX.com")

![\[= \beta ^{ind}_{asset} \frac{1-\frac{V^{proj}_{fix}}{V^{proj}_{asset}}}{1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2e59a7922907e0e1cf633939c849f6b1_l3.png "Rendered by QuickLaTeX.com")

![\[\beta^{project}_{asset}=1.0 \left( 1+ \frac {1000}{200} \right)=6\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e757d8c2543eaf64339e1fdf4bef1aed_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{P}=\frac{R}{R-C}\beta_{R} - \frac{C}{R-C}\beta_{C}=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-214f6b4aa833f50c0348169b35112362_l3.png "Rendered by QuickLaTeX.com")

![\[=\frac{1200}{1200-1000}1 - \frac{1000}{1200-1000}0=6\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-58210695bcd89b8fbc6f9c8b560ad8fa_l3.png "Rendered by QuickLaTeX.com")

, variable costs

, variable costs  and revenues

and revenues  cannot be found easily. But we can try to approximate them with P&L or balance sheet figures, which are available more eaysily. Let us consider eternal yearly revenues

cannot be found easily. But we can try to approximate them with P&L or balance sheet figures, which are available more eaysily. Let us consider eternal yearly revenues  , yearly fixed costs

, yearly fixed costs  and yearly variable costs

and yearly variable costs  . The risk free rate is

. The risk free rate is ![\[\beta _{asset} = \beta_{rev} \left( 1 - \frac{V_{fix}}{V_{asset}} \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1dfd5750e036dfe0ed0c2580165d58d1_l3.png "Rendered by QuickLaTeX.com")

![\[V_{fix}=- \frac{\alpha R}{r_f}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8c2173bb867d2039c7c24b01280886db_l3.png "Rendered by QuickLaTeX.com")

![\[V_{asset}= \frac{R - \alpha R - \beta R}{r_m}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2047a4c2ba3b0169ee09b36933d3035a_l3.png "Rendered by QuickLaTeX.com")

:

:![\[\beta _{asset} = \beta_{rev} \left( 1 + \frac{\frac{\alpha R}{r_f}}{\frac{R - \alpha R - \beta R}{r_m}} \right) = \beta_{rev} \left( 1 + \frac{r_m}{r_f}\frac{\alpha}{1-\alpha-\beta} \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2d2c815f15ff7b3feca76b5a7bb8316c_l3.png "Rendered by QuickLaTeX.com")

and

and  approximately, so

approximately, so  ,

,  is the ratio of annual fixed costs to annual profit. That means that you have to multiply that factor with the 2, when applying P&L figures in approximation and not present values.

is the ratio of annual fixed costs to annual profit. That means that you have to multiply that factor with the 2, when applying P&L figures in approximation and not present values.  of an option at time

of an option at time  is given by:

is given by:![\[C_0=\frac{\alpha C_{u,t_1}+(1-\alpha )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d245e3e501c03334a52b0327fc44aea3_l3.png "Rendered by QuickLaTeX.com")

and

and  are the option values of the up and down development at time

are the option values of the up and down development at time  .

.  is the risk free rate and T is the time between

is the risk free rate and T is the time between  ,

,  .

.  is the risk neutral probability of the up movement in

is the risk neutral probability of the up movement in  is the risk neutral probability of the down movement in

is the risk neutral probability of the down movement in ![\[\alpha=\frac{(1+r)^T-d}{u-d}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-53e84d5ecdafd962f48030489a62864d_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{\frac{(1+r)^T-d}{u-d} C_{u,t_1}+(1-\frac{(1+r)^T-d}{u-d} )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-4585ecf3307b3ea36a992a134bd156a8_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{( (1+r)^T-d ) C_{u,t_1}+(u-(1+r)^T )C_{d,t_1}}{(1+r)^T (u-d)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e41bd7434143afaf1fc36677db98383c_l3.png "Rendered by QuickLaTeX.com")

and

and  :

:![\[u= \frac{EV(S_{t_0})}{S_{u,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d9deab9057d9c6d1f3a1ba8f0e6ce779_l3.png "Rendered by QuickLaTeX.com")

![\[d= \frac{EV(S_{t_0})}{S_{d,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-875c14eb30bf1a7d78b5173c9c6dfadf_l3.png "Rendered by QuickLaTeX.com")

and down state

and down state  have not occured. Many times that leads to the argument that these probabilities do not influence the option value. But that is not true. The expected value of the state

have not occured. Many times that leads to the argument that these probabilities do not influence the option value. But that is not true. The expected value of the state  and therefore

and therefore  depends on the probabilities. The expected value of the event state in

depends on the probabilities. The expected value of the event state in ![\[EV(S_{t_0})=\frac{EV(S_{t_1})}{(1+D)^T}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{(1+D)^T}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1bde57d477d9f69bdf954feb24df97ba_l3.png "Rendered by QuickLaTeX.com")

![\[u=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{u,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ba3a6fc511e4ae945efcc80c544226d2_l3.png "Rendered by QuickLaTeX.com")

![\[d=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-df6488617bbde3eaabec1cf22b39708f_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{( (1+r)^T-\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}) C_{u,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}+\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0769b16c961ea4a991747ee6dec7ad23_l3.png "Rendered by QuickLaTeX.com")

![\[+\frac{(\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-(1+r)^T )C_{d,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5b78a3049855170fe758d7f83b5e5355_l3.png "Rendered by QuickLaTeX.com")

of the up state

of the up state  , and

, and  of the down state

of the down state  respectively. That is what we wanted to prove. The argument that this dependency does not exist, does not take into account that the value of state

respectively. That is what we wanted to prove. The argument that this dependency does not exist, does not take into account that the value of state  depends on the state probabilities in

depends on the state probabilities in  for the buying and

for the buying and  for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.

for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.![\[NPV_b=\sum_{i}^{}\gamma_{b,i}C_{b,i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7edf54aa8061c21fae0649b7cb42febf_l3.png "Rendered by QuickLaTeX.com")

![\[NPV_l=\sum_{j}^{}\gamma_{l,j}C_{l,j}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2ff141704520007119cf9e00400279cc_l3.png "Rendered by QuickLaTeX.com")

.

. ,

,  , which is the sum of different assets values

, which is the sum of different assets values  :

:![\[C(t)=\sum_{i}^{}C_i(t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-238c5682b36c90200f3872ee0001a260_l3.png "Rendered by QuickLaTeX.com")

the asset values are

the asset values are  and

and  with

with  . The asset value

. The asset value  is developing in time

is developing in time  , that means:

, that means:![\[C_i (t)=C_i(0)exp(r_i t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-199dec8af5bafc55f69c19ffd13b2d2b_l3.png "Rendered by QuickLaTeX.com")

. Setting

. Setting  we obtain:

we obtain:![\[r=\frac{1}{t}ln\frac{C(t)}{C(0)}=\frac{1}{t}ln\left( \sum_{i}^{} \left \frac{C_i(0)}{C(0)} exp \left( r_i t \right) \right \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fb659cb84b82fa3fac2f0009b503dd4b_l3.png "Rendered by QuickLaTeX.com")

and

and  . Hence we get a first order approximation of

. Hence we get a first order approximation of ![\[r\simeq \frac{1}{t}\left( \sum_{i}^{} \left( \frac{C_i(0)}{C(0)} \left( 1+ r_i t \right) \right) -1 \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-87db3d07482630425a989b6495027b30_l3.png "Rendered by QuickLaTeX.com")

![\[r\simeq \sum_{i}^{} \frac{C_i(0)}{C(0)} r_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5806f016a86a9e819753e1a5e6579448_l3.png "Rendered by QuickLaTeX.com")

return rate

return rate ![\[WACC=r=\frac{D}{E+D}r_D+\frac{E}{E+D}r_E\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7b9fcbf01c1f74e6a122461f37027337_l3.png "Rendered by QuickLaTeX.com")

or

or  . With a substitution of

. With a substitution of  , you can transform these two return rates into each other.

, you can transform these two return rates into each other. , is the sum of revenues’ value,

, is the sum of revenues’ value, ![\[V_{asset}=V_{rev}+V_{var}+V_{fix}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cf23103bfba3ed586bd4ee1464a7b4d8_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{asset}=\frac{\beta_{rev} V_{rev} + \beta_{var} V_{var}+ \beta_{fix} V_{fix}}{V_{asset}}.\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f9abbfbe3a34248c1ea171096730d969_l3.png "Rendered by QuickLaTeX.com")

and therefore

and therefore  . We obtain:

. We obtain:![\[\beta_{asset}=\frac{V_{rev}\beta_{rev} + V_{var}\beta_{var}}{V_{asset}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c8bd7662c544e7ee1cc1dfd493bc7da0_l3.png "Rendered by QuickLaTeX.com")

. We get:

. We get:![\[\beta_{asset}=\beta_{rev} \frac{V_{rev} + V_{var}}{V_{asset}}=\beta_{rev} \left( 1-\frac{V_{fix}}{V_{asset}} \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-460385135a1bed426f4e8cc7f7cb9662_l3.png "Rendered by QuickLaTeX.com")

, and the value of the asset is positive,

, and the value of the asset is positive,  , in ordinary cases. The expression in the bracket becomes

, in ordinary cases. The expression in the bracket becomes  . That means that the beta of the asset is higher than the beta of the revenues,

. That means that the beta of the asset is higher than the beta of the revenues,  . Obviously that is true, because adding fixed costs increases the beta of the asset. This effect is known as operating leverage.

. Obviously that is true, because adding fixed costs increases the beta of the asset. This effect is known as operating leverage. and

and  .

. ![\[r_E=r_f+\beta _{rev}\left( r_m - r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-333b7bf948d2e673718fe660bee9b387_l3.png "Rendered by QuickLaTeX.com")

considering debt

considering debt ![\[r_{rev}=\frac{D}{E+D} \left( 1-t \right) r_D + \frac{E}{E+D} r_E\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8816ce85e3ebb914b2b3b891bb1d463d_l3.png "Rendered by QuickLaTeX.com")

, divided by the present value of all investment cash flows,

, divided by the present value of all investment cash flows,  . Hereby it is important how we define the term investment. You can have a look at my proposal in this

. Hereby it is important how we define the term investment. You can have a look at my proposal in this ![\[PI=\frac{PV_C}{PV_I}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f8912a2a1acef3578476fece21ce73f7_l3.png "Rendered by QuickLaTeX.com")

shows how much value is created per investment. All projects with a

shows how much value is created per investment. All projects with a  are creating additional value to the investors, all projects with a

are creating additional value to the investors, all projects with a  are destroying value.

are destroying value.![\[PI^*=\frac{PV_C-PV_I}{PV_I}=\frac{PV_C}{PV_I}-1=PI-1\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-852d8bdcfe0d8e08d8e4e08ea95efc33_l3.png "Rendered by QuickLaTeX.com")

:

:![\[PIA=\frac{PI}{A_{n,r}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cae3fb545351871cad5018e3c01b814b_l3.png "Rendered by QuickLaTeX.com")

![\[A_{n,r}=\frac{1}{r}\left( 1-\frac{1}{\left( 1+r \right)^n} \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bb804176bdcf6a6e5abb0a6b97de6a61_l3.png "Rendered by QuickLaTeX.com")

![\[I_t^{res}:=f_t+c_t-c_{t-1}-c_{t-1}i_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bc65d4df301a3c2e176603cf8e26139f_l3.png "Rendered by QuickLaTeX.com")

is the cash flow in period

is the cash flow in period  the fixed capital in period

the fixed capital in period  the discount rate in period

the discount rate in period  is just the depreciation in period

is just the depreciation in period ![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}(1+i_t)-c_t)\rho_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-69a2df2c6eec9bcf4204b280e7e4d618_l3.png "Rendered by QuickLaTeX.com")

is the discount factor in period

is the discount factor in period  . That means

. That means  . With that we obtain:

. With that we obtain:![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}\rho_{t-1} - c_t \rho_t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-80f028ea0a1e5aa789c7c681959a662b_l3.png "Rendered by QuickLaTeX.com")

. And if all fixed asset is depreciated in the considered n periods, we can set

. And if all fixed asset is depreciated in the considered n periods, we can set  . With these two premises we realize that all terms of the sum become zero.

. With these two premises we realize that all terms of the sum become zero.![\[\sum_{t=0}^{n}(f_t-I_t^{res}) \rho_t = c_{-1} \rho_{-1} - c_n \rho_n=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-97221d236f91df1aa277ca8486b5c86b_l3.png "Rendered by QuickLaTeX.com")

. The discount factors

. The discount factors  can be different for each cach flow

can be different for each cach flow ![\[NPV=\sum_{i}^{}\gamma _i c_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-be714489173707f0b2e1b021beec0ef7_l3.png "Rendered by QuickLaTeX.com")

(uniformity). Let

(uniformity). Let ![\[NPV=\sum_{t}^{}\gamma _t C_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-34fe10e182bb18789975d41fbebb21cb_l3.png "Rendered by QuickLaTeX.com")

has polynomial character in

has polynomial character in ![\[NPV=\sum_{t}^{}C_t\gamma ^t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6e05f66d719263443df328c80a352a1f_l3.png "Rendered by QuickLaTeX.com")

we get the well-known formula:

we get the well-known formula:![\[NPV=\sum_{t}^{}C_t\left( 1+i \right) ^{-t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f21d29c636ae7845b1eb805b47a261df_l3.png "Rendered by QuickLaTeX.com")

is now defined to be the values of

is now defined to be the values of ![\[NPV=\sum_{t}^{}C_t\left( 1+i^{IRR} \right) ^{-t}=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-058630d81fc54ddadec91380bef860e6_l3.png "Rendered by QuickLaTeX.com")

are calculated by adding risk premiums to the risk-free rate. Considering the Capital Asset Pricing Model (CAPM) the expected value of the equity return rate is:

are calculated by adding risk premiums to the risk-free rate. Considering the Capital Asset Pricing Model (CAPM) the expected value of the equity return rate is:![\[E \left( r_e \right)= r_f+\beta \left( E\left( r_m \right) - r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-38e62fabc01a82f5db7e3983991acc6e_l3.png "Rendered by QuickLaTeX.com")

of the valuation. But be aware that this is an approximation and can be false in some cases.

of the valuation. But be aware that this is an approximation and can be false in some cases. having annual return rates

having annual return rates  and standard deviations of the annual return rates

and standard deviations of the annual return rates  . The variance of the portfolio return rate is given by:

. The variance of the portfolio return rate is given by:![\[var\left( R_P \right)=\sum_{i}^{}x_i\text{cov}\left( R_i, R_P \right) \text{, or}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-213e53714645a6928f8809c075b35994_l3.png "Rendered by QuickLaTeX.com")

![\[ var\left( R_P \right) =\sum_{i}^{}x_i\sigma\left( R_i \right)\sigma\left( R_P \right)\text{corr}\left( R_i, R_P \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-89d31827c4e75a2404edbcb4707fbdcc_l3.png "Rendered by QuickLaTeX.com")

gives the standard deviation

gives the standard deviation ![\[\sigma\left( R_P \right)=\sum_{i}^{}x_i\sigma\left( R_i \right)\text{corr}\left( R_i, R_P \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-db9c91da9142d49d0592f3f742409da5_l3.png "Rendered by QuickLaTeX.com")

.

.![\[\frac{E\left( R_P\right)-r_f}{\sigma \left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-45e12ba3a38d9bebc05f90ab64f78c59_l3.png "Rendered by QuickLaTeX.com")

is the expected value of

is the expected value of  and

and ![\[\text{E}\left( R_i \right)-r_f > \sigma\left( R_i \right)\text{corr}\left( R_i,R_P \right)\frac{E\left( R_P\right)-r_f}{\sigma\left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-90f6b90208a26c8b429370ea22e0168b_l3.png "Rendered by QuickLaTeX.com")

of the new investment to the existing portfolio:

of the new investment to the existing portfolio:![\[\beta_i^P=\frac{\sigma\left( R_i \right)\text{corr}\left( R_i,R_P \right)}{\sigma\left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-604cc66ff63230e502c823c1520bc1b2_l3.png "Rendered by QuickLaTeX.com")

![\[\text{E}\left( R_i \right) > r_f+\beta_i^P\left( E\left( R_P\right)-r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-750ab8b8d312bc0ee256f6103ec6e4fb_l3.png "Rendered by QuickLaTeX.com")

![\[ r_i = r_f+\beta_i^P\left( E\left( R_P\right)-r_f \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fc1f59b1f6bff846398674e4242b6bbb_l3.png "Rendered by QuickLaTeX.com")

. The sign of NPV indicates whether an asset generates value to the fund providers (debt and equity) or not. If only the amount, but not the sign of NPV changes by a time shift, the decision to allocate the project or not does not change. That means that the decision itself does not depend on the time scale. In many books I have read that argument. But is this really true?

. The sign of NPV indicates whether an asset generates value to the fund providers (debt and equity) or not. If only the amount, but not the sign of NPV changes by a time shift, the decision to allocate the project or not does not change. That means that the decision itself does not depend on the time scale. In many books I have read that argument. But is this really true? we can write

we can write  instead of

instead of  . The NPV of the project at the “present” time

. The NPV of the project at the “present” time  , is:

, is:![\[NPV_0=\sum_{i}^{}E(C_i) e^{-\alpha t_i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-210d871123a0c687f1a41a644f034588_l3.png "Rendered by QuickLaTeX.com")

is the expected value of the i-th cash flow component. When we shift time by

is the expected value of the i-th cash flow component. When we shift time by  :

:![\[NPV_ {\Delta t} =\sum_{i}^{}E(C_i) e^{-\alpha (t_i+ {\Delta t} )}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-9004eb4b37f2bef2f6809e94c349a420_l3.png "Rendered by QuickLaTeX.com")

![\[ NPV_ {\Delta t} = e^{ -\alpha \Delta t} \sum_{i}^{}E(C_i) e^{-\alpha (t_i )}= e^{ -\alpha \Delta t} NPV_0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-03541590c7a5b90db51ed95302ab6383_l3.png "Rendered by QuickLaTeX.com")

, the sign of

, the sign of  respectively, for cash flow

respectively, for cash flow ![\[NPV_0=\sum_{i}^{}E(C_i) e^{-\alpha_i t_i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-19b1f47cb1ceb032a87c531f81c1d140_l3.png "Rendered by QuickLaTeX.com")

![\[NPV_ {\Delta t} =\sum_{i}^{}E(C_i) e^{-\alpha_i (t_i+ {\Delta t} )}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1378ee94d492c34b8db2e3d644f37a21_l3.png "Rendered by QuickLaTeX.com")