Problem Framing

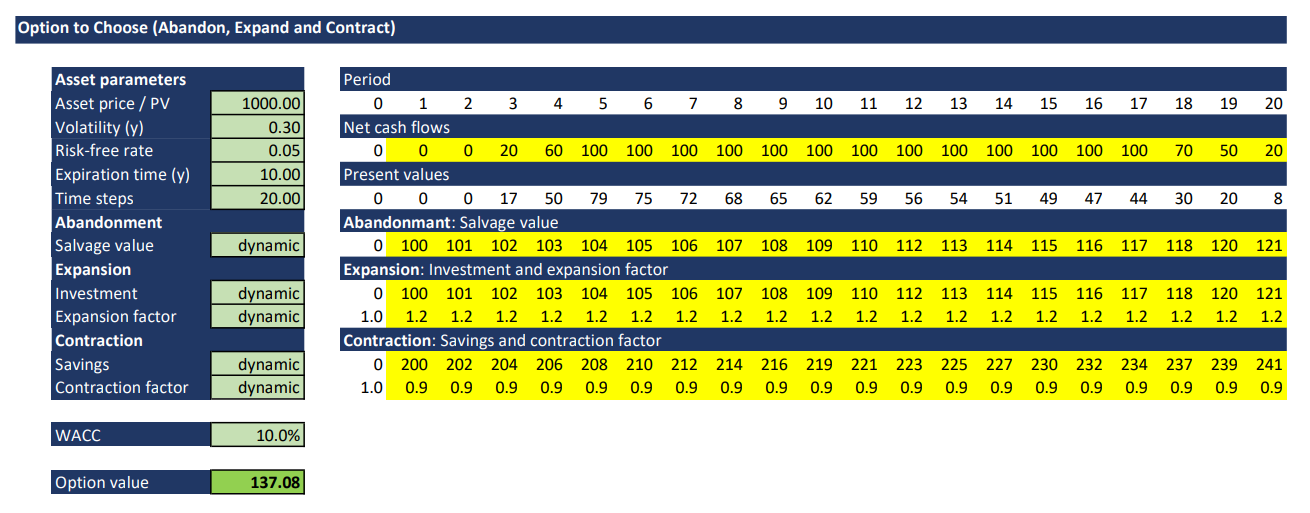

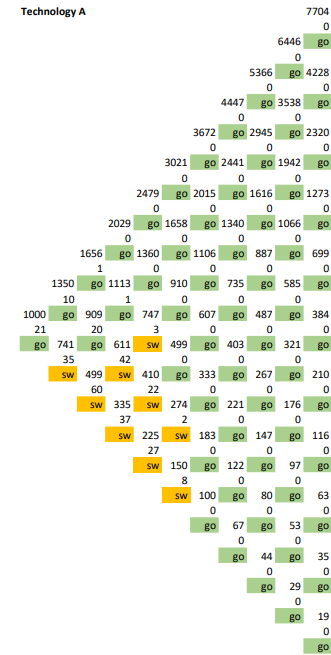

In this post I want to give a simple example of a choose option valuation. The considered project lasts 10 years, the WACC of the contribution (market) cash flows is 10.0% and constant over time. The contribution cash flows are shown in the graph below. Let the risk free rate be 5.0%. The project provides 3 options: 1) Option to expand with an investment of 100 kEUR (increasing with an inflation rate of 2% per year). The contribution cash flows would be increased by 20%, if managements invests in the expansion. 2) Option to abandon the project with a salvage value of 100 kEUR (increasing with an inflation rate of 2% per year) and 3) Option to contract with a savings of 200 kEUR (increasing with an inflation rate of 2% per year) and a contraction factor of 0.9. DCF analysis provides a present value of the market contribution cash flows of 1 million EUR. A Monte-Carlo-Simulation shows a project volatility of 0.30. We analyze this choose option with the binomial approach of Cox-Ross-Rubinstein. As time periods we take two time steps per year, so that you can read the figures in the lattice properly. For higher accuracy we could take smaller time periods anytime.

Choose Option Valuation

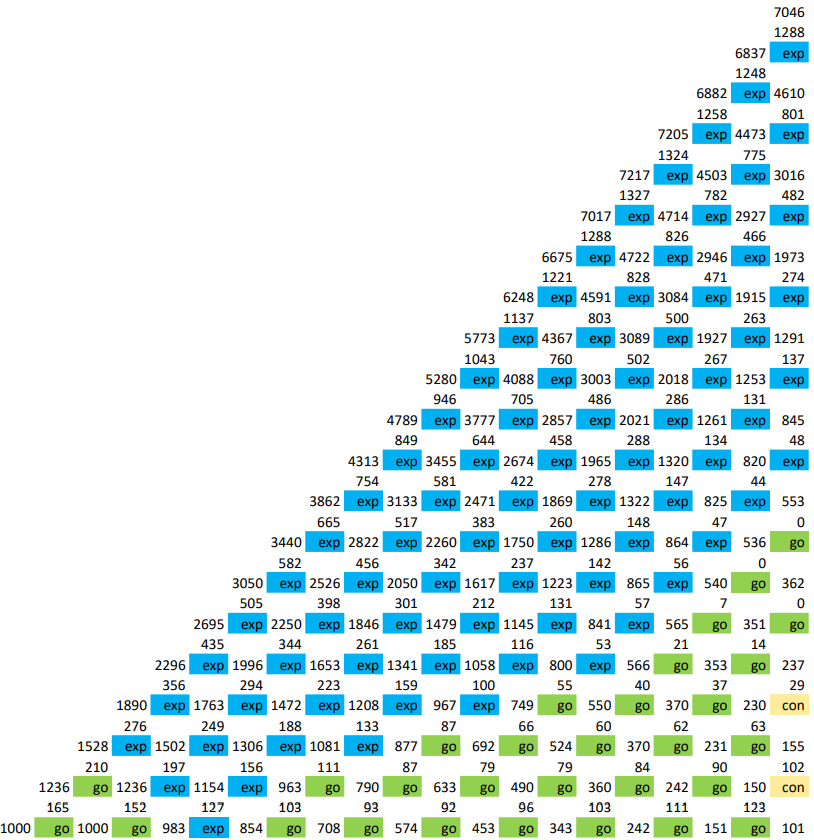

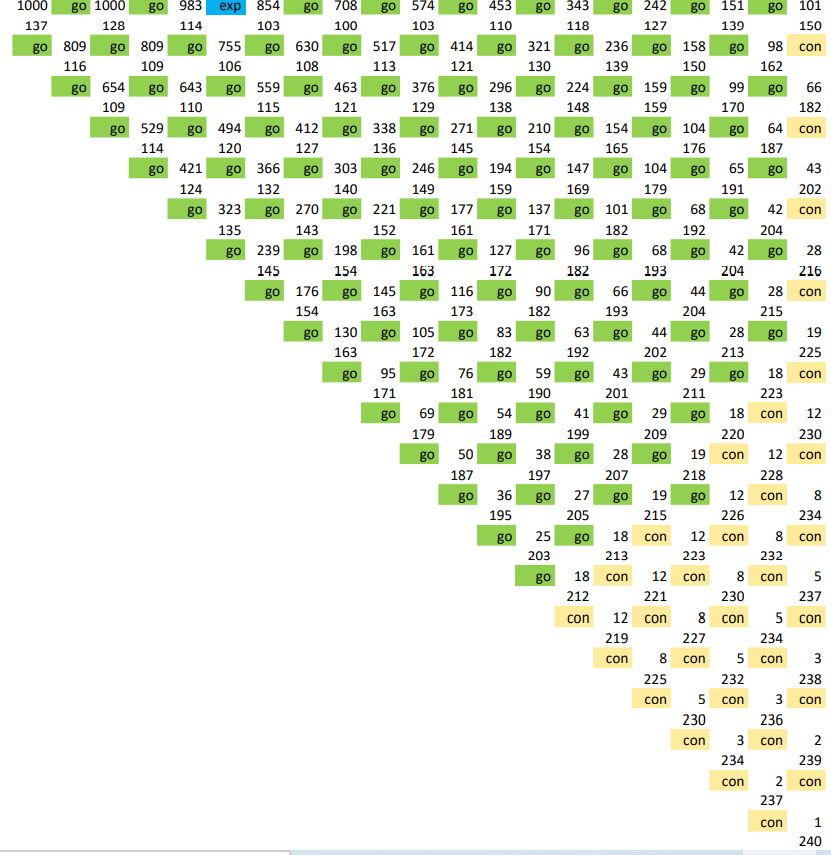

We want to give answers to the following questions: What is the value of this option to choose? When do we have to take which option to get the maximum value added for the project?

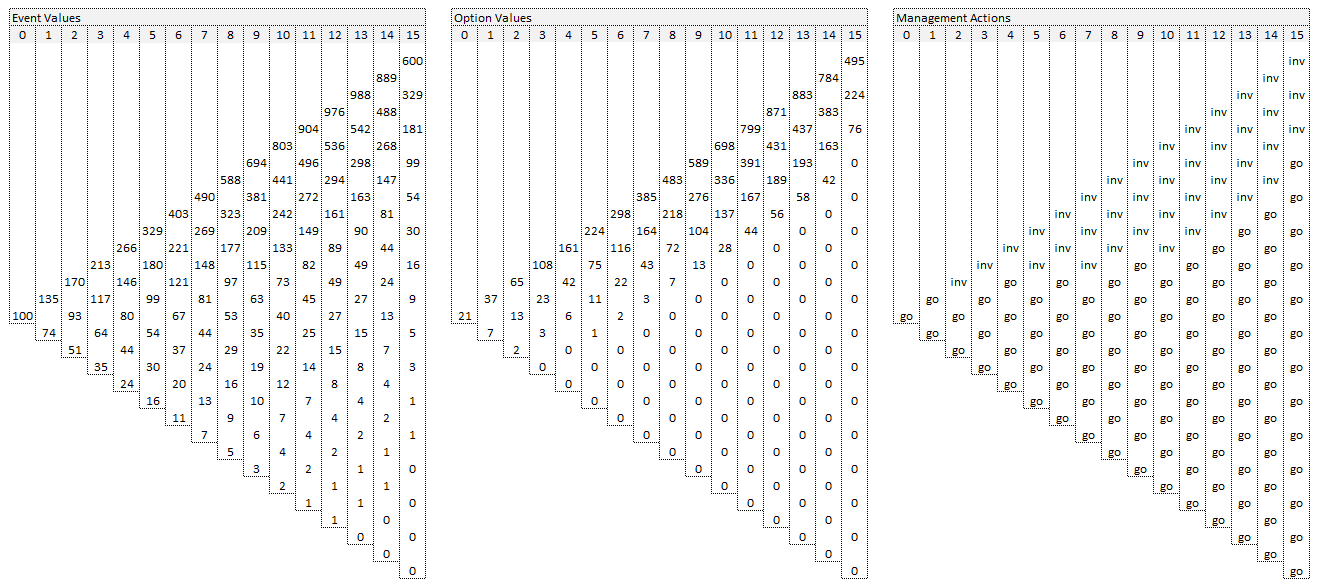

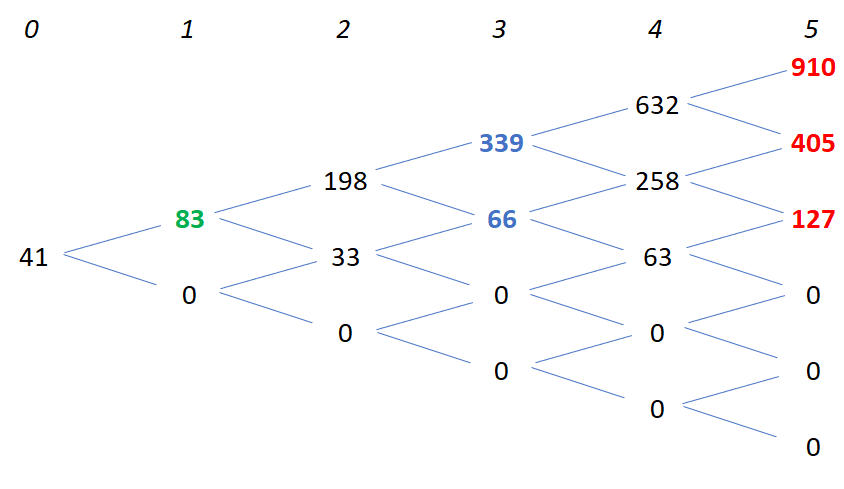

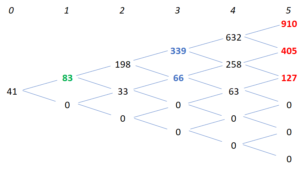

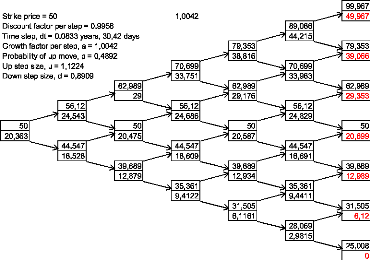

We take the binomial approach from Cox-Ross-Rubinstein to solve that issue. Following you can have look at the binomial lattice. The first value of each node is the value of the underlying (market contribution cash flows). The sevond value is the value of the options at this node. In the third line you can see whether you have to take an option and which option you have to take. “exp” means to invest in the expansion of the project, “go” means to take no option at this node and “con” means to invest in the contraction of the project.

The total value of the three options is 137 kEUR. That is the maximum investment that should be done for the three options in sum. The option to abandon is not taken in any node. That means that you should not invest in this abandonment option. In the first year you should not take any option, let the project evolve. In the second year there might be the first opportunities to take the expansion option. In the following years the expansion option is a good opportunity in case of positive cash flow development. Your project controlling should have a look at the cash flow development and go the right path through the lattice over time. In the first six years the contraction option provides no addition value to the project. But in the last three years of the project the contraction option becomes more important.

Note that this choose option adds a value of 137 kEUR to the project. That means that the NPV of the classical DCF analysis can convert from negative to positive because of the additional value. That could lead to a reconsidering of the project decision. The ENPV (expandedNPV) is the NPV of the project plus the value of the choose option.

Additional Remarks

I constructed the event tree from the project’s contribution cash flow volatility out of a Monte-Carlo-Simulations. Of course you can also create the nodes of the event trees by calculating the time values of the outstanding contribution cash flows explicitly. Discussion with management and marketing can provide the required cash flows and probabilities of the event tree.

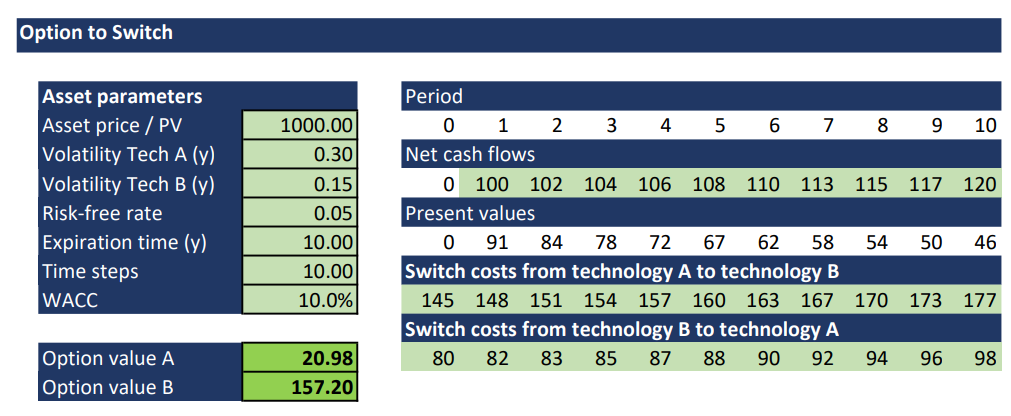

This option to choose combines the three options of expansion, contraction and abandonment. This example also shows that the value of various options is not the sum of its individual options. Although the option to abandon has an option value by itself, it contributes no additional value to the option to choose, because it is not required in any node. Analytical valuation methods like Black-Scholes-Merton cannot provide exact solutions for such interdependent options.

be the value of the underlying asset in

be the value of the underlying asset in  . In a project or investment this might be the present value of the project’s contribution (market related) cash flows. The positive development of

. In a project or investment this might be the present value of the project’s contribution (market related) cash flows. The positive development of  ,

,  , occurs with probability

, occurs with probability  , the negative development with value

, the negative development with value  in

in  . The twin security of the underlying in the open market takes a similar notation

. The twin security of the underlying in the open market takes a similar notation  ,

,  ,

,  ,

, in

in  in the upper state

in the upper state  in the lower state

in the lower state  .

. shares of twin security

shares of twin security  at the risk-free rate

at the risk-free rate  . The values of the upper and lower state in

. The values of the upper and lower state in  and

and  .

. must be the same in the upper and in the lower state. Setting

must be the same in the upper and in the lower state. Setting  we get:

we get:![\[n=\frac{E^+-E^-}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0f1b9697c29529cdc9d6fb23d9232485_l3.png "Rendered by QuickLaTeX.com")

![\[B=\frac{1}{1+r}\frac{{E^+S^--E}^-S^+}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ac35b5d4ad5fc53d32028c8dc64933fd_l3.png "Rendered by QuickLaTeX.com")

. With that we calculate the value of the option in

. With that we calculate the value of the option in ![\[E=\frac{\left(\frac{S\left(1+r\right)-S^-}{S^+-S^-}\right)E^++\left(1-\frac{S\left(1+r\right)-S^-}{S^+-S^-}\right)E^-}{1+r}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bccf07b0c1c2c9b722c78bf7bd5bfd44_l3.png "Rendered by QuickLaTeX.com")

to simplify the previous expression.

to simplify the previous expression.![\[p^\prime=\frac{S\left(1+r\right)-S^-}{S^+-S^-}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a79fb856ce26df70c2d45b3cf96f8461_l3.png "Rendered by QuickLaTeX.com")

![\[E=\frac{p\prime E^++\left(1-p\prime\right)E^-}{1+r}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-05a980182c7265f624712db1703bf91c_l3.png "Rendered by QuickLaTeX.com")

for

for ![\[VU+VTS=E+D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-b94e9cb916ccb4f26a54e3b9856e56c1_l3.png "Rendered by QuickLaTeX.com")

![\[r_A\frac{VU}{VU+VTS}+r_{TS}\frac{VTS}{VU+VTS}=r_E\frac{E}{E+D}+r_D\frac{D}{E+D}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ba7175f24e5d2d722cf9eb48a3d5a251_l3.png "Rendered by QuickLaTeX.com")

![\[r_E=r_A+\left(r_A-r_D\right)\frac{D}{E}-\left(r_A-r_{TS}\right)\frac{VTS}{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c4a38630c0ddc68d3533f60cd60f0d12_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_E=\beta_A+\left(\beta_A-\beta_D\right)\frac{D}{E}-\left(\beta_A-\beta_{TS}\right)\frac{VTS}{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ff2295b7bcf29a5487fd7538a25bee1a_l3.png "Rendered by QuickLaTeX.com")

. If the tax shield savings are proportional to the taxes paid (see

. If the tax shield savings are proportional to the taxes paid (see ![\[WACC=r_E\frac{E}{E+D}+r_D\left(1-T_C\right)\frac{D}{E+D}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7918e343e7bc7ac58ac623007abcc0a9_l3.png "Rendered by QuickLaTeX.com")

![\[WACC=r_A\left(1-\frac{VTS}{V}\right)-r_DT_C\frac{D}{V}+r_{TS}\frac{VTS}{V}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-9175aaf5f085ae56e03f707897df67a3_l3.png "Rendered by QuickLaTeX.com")

,

,  ,

,  are the return rates of the unlevered asset, debt and tax shield. V and VTS are the values of the levered firm and the tax shield. D is the amount of debt, V is the value of the levered firm, namely the sum of equity and debt.

are the return rates of the unlevered asset, debt and tax shield. V and VTS are the values of the levered firm and the tax shield. D is the amount of debt, V is the value of the levered firm, namely the sum of equity and debt.

![\[VTS=\sum_{j=1}^{\infty}{DT_C\left(\frac{1}{1+r_D}\right)}^j=\frac{DT_C}{r_D}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d169ad8bf7a35016ef591669bce33651_l3.png "Rendered by QuickLaTeX.com")

![\[r_E=r_A+\left(r_A-r_D\right)\frac{D}{E}\left(1-T_C\right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6fa58bdfd3eb0dc6d641d45343c1b3a6_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_E=\beta_A+\left(\beta_A-\beta_D\right)\frac{D}{E}\left(1-T_C\right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e04c0df60039253416a23b6066f9e89e_l3.png "Rendered by QuickLaTeX.com")

![\[WACC=r_A\left(1-T_C\frac{D}{E+D}\right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-79388769c61d5bf8f89d5f9eda40df7e_l3.png "Rendered by QuickLaTeX.com")

. Hence we get the well-known Hamada equation for levered beta:

. Hence we get the well-known Hamada equation for levered beta:![\[\beta_E=\beta_A\left(1+\frac{D}{E}\left(1-T_C\right)\right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7f403c116e10e4cb675c051d48693b12_l3.png "Rendered by QuickLaTeX.com")

.

.![\[r_E=r_A+\left(r_A-r_D\right)\frac{D}{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2e59b5cd164faaa326ceaf83f50110be_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_E=\beta_A+\left(\beta_A-\beta_D\right)\frac{D}{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-35627d382de9e7f451cbae396380d92a_l3.png "Rendered by QuickLaTeX.com")

![\[WACC=r_A-r_DT_C\frac{D}{E+D}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-29404c1c3e2ceaf88a41cb8e2b52aa4d_l3.png "Rendered by QuickLaTeX.com")

![\[{VTS}^{ME}=\frac{Dr_DT_C\left(1+r_A\right)}{\left(r_A-g\right)\left(1+r_D\right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-dc553a9d0a405871c2d5012e8a2341cf_l3.png "Rendered by QuickLaTeX.com")

equal to

equal to  :

:![\[{VTS}^{HP}=\frac{Dr_DT_C}{\left(r_A-g\right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-35260db8c295e740eb5cb50c4bdbd8b0_l3.png "Rendered by QuickLaTeX.com")

![\[MIRR=\sqrt[n]{\frac{\text{FV(contribution cash flows,WACC)}}{\text{PV(invest cash flows, financing rate)}}}-1\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bc3151b9811774776aaad69dd41965ad_l3.png "Rendered by QuickLaTeX.com")

, the Baldwin rate can decrease. This is because the number of periods increases and the value of the root decreases. Cases that lead to wrong results are not acceptable for decision key figure.

, the Baldwin rate can decrease. This is because the number of periods increases and the value of the root decreases. Cases that lead to wrong results are not acceptable for decision key figure. , is the sum of its cash flows’ (present) values, namely revenue

, is the sum of its cash flows’ (present) values, namely revenue  , variable costs

, variable costs  and fixed costs,

and fixed costs,  . Present values are linear, for the value of the asset we can write:

. Present values are linear, for the value of the asset we can write:![\[V_{asset} = V_{rev} + V_{fix} + V_{var}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-06ecb79ed1504240a5e293b161ef7729_l3.png "Rendered by QuickLaTeX.com")

![\[V_{rev} = V_{asset} - V_{var} - V_{fix}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a2fa990f707942325d457ca9960f0312_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{rev}=\beta_{asset}\frac{V_{asset}}{V_{rev}}-\beta_{var}\frac{V_{var}}{V_{rev}}-\beta_{fix}\frac{V_{fix}}{V_{rev}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-48440be08a93eba8c9e4d72f82af4e04_l3.png "Rendered by QuickLaTeX.com")

. The betas of revenues and variable expenses are more or less the same, because they are both related to the output. Therefore we can substitute

. The betas of revenues and variable expenses are more or less the same, because they are both related to the output. Therefore we can substitute  for

for  .

. ![\[\beta_{asset}=\beta_{rev}\frac{V_{rev}+V_{var}}{V_{asset}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a07bb844c7de6245a10dca66db97ab1c_l3.png "Rendered by QuickLaTeX.com")

we obtain:

we obtain:

![\[\beta_{asset}=\beta_{rev} \left( 1 - \frac{V_{fix}}{V_{asset}} \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cf2bade4223c37c2fd06d93ee6c5e958_l3.png "Rendered by QuickLaTeX.com")

![\[\text{DOL}= 1 + \frac{\left| \text{fixed exp.} \right| }{\text{profits}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5631e58f9f60adde3e5596caafc027ab_l3.png "Rendered by QuickLaTeX.com")

is the same for all companies in the industry segment.

is the same for all companies in the industry segment.  is the average asset beta of the industry segment, which has an average ratio of fixed expenses to profits.

is the average asset beta of the industry segment, which has an average ratio of fixed expenses to profits.  … after-tax discount rate

… after-tax discount rate … rate of debt to sum of equity

… rate of debt to sum of equity  ,

,

… equity interest rate

… equity interest rate … marginal corporate tax rate

… marginal corporate tax rate![\[r=\left( 1-L \right)r_{E}+Lr_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e27f6e854c47d27bb1651ad6e45e2bde_l3.png "Rendered by QuickLaTeX.com")

we have:

we have:![\[r_{E}=\frac{r-Lr_D}{1-L}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8cdf8fee024408f1a475932c0da21d94_l3.png "Rendered by QuickLaTeX.com")

![\[r^{*}=\left( 1-L \right)r_{E}+L\left( 1-t \right)r_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f19765a904cf1b8b48832af962b2c107_l3.png "Rendered by QuickLaTeX.com")

![\[r^{*}= r -Ltr_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-95ee3f0f11e1c330099229798f192ac0_l3.png "Rendered by QuickLaTeX.com")