Joachim Kuczynski, 14 November 2025

This article shows how to derive the WACC (weighted average cost of capital) of a project from the WACC of a company (or asset portfolio in general). Further on company and portfolio have the same meaning. Let us assume a company or portfolio with  projects. The relative share of project

projects. The relative share of project  in the portfolio is

in the portfolio is  . The WACC of project is

. The WACC of project is  . The cost of capital of the portfolio,

. The cost of capital of the portfolio,  , is given by:

, is given by:

(1)

That means that the WACC of a portfolio is the weighted average of the components’ WACC.

Let us have a look at the variance of the portfolio WACC:

(2)

The covariance is bilinear, we get:

(3)

The correlation of an asset’s WACC with the portfolio’s WACC is defined by:

(4)

and

and  are the standard deviations of and . Substituting covariance by correlation we get:

are the standard deviations of and . Substituting covariance by correlation we get:

(5)

Dividing by the standard deviation  leads us to the standard deviation of the portfolio:

leads us to the standard deviation of the portfolio:

(6)

That means that the incremental risk contribution of each project to the risk of the portfolio is  and not just the weighted sum of its projects’ risks. Hence we can e.g. reduce the WACC of the portfolio by adding a project with negative correlation to the portfolio.\

and not just the weighted sum of its projects’ risks. Hence we can e.g. reduce the WACC of the portfolio by adding a project with negative correlation to the portfolio.\

Instead of including a new project to the portfolio the company can also increase the return of the portfolio by increasing the risk of the portfolio. This reward-to-volatility ratio of the tangential portfolio is given by the Sharpe Ratio:

(7)

is the expected value of and

is the expected value of and  is the after-tax debt interest rate. The company wants to invest in the new project, if the additional WACC of this project is lower than an investment in the existing portfolio with the same risk changes. Hence we obtain the requirement to invest in the new project:

is the after-tax debt interest rate. The company wants to invest in the new project, if the additional WACC of this project is lower than an investment in the existing portfolio with the same risk changes. Hence we obtain the requirement to invest in the new project:

(8)

With that we can define the sensitivity  of the new project to the existing portfolio:

of the new project to the existing portfolio:

(9)

Substituting with the requirement for the new investment becomes the well-known equation:

(10)

With that we can define a maximum annual WACC of the additional project. This is the maximum WACC at which a company would decide to invest in the project.

(11)

Let us assume that the new project and the company are correlated completely, which means  . In this case we get:

. In this case we get:

(12)

The quotient  is called relative risk factor of project . The risk premium of the company WACC is adapted by the quotient of the standard deviations of the project and the company. The higher the risk of the project the higher the required WACC of the project to become a new part of the company portfolio. If the risk of the project and the risk of the company are the same, the WACC of the project and the company are the same, too. The standard deviation can be generated by Monte Carlo Simulation or approximated by best/worst case scenarios. Another approach is to estimate the standard deviations by management. Instead of comparing the project to the whole company portfolio we can also compare it to a benchmark project. This benckmark project is considered to be representative for the company.

is called relative risk factor of project . The risk premium of the company WACC is adapted by the quotient of the standard deviations of the project and the company. The higher the risk of the project the higher the required WACC of the project to become a new part of the company portfolio. If the risk of the project and the risk of the company are the same, the WACC of the project and the company are the same, too. The standard deviation can be generated by Monte Carlo Simulation or approximated by best/worst case scenarios. Another approach is to estimate the standard deviations by management. Instead of comparing the project to the whole company portfolio we can also compare it to a benchmark project. This benckmark project is considered to be representative for the company.

and equity return rates

and equity return rates  .

.  data pairs.

data pairs.  and

and  are the arithmetic mean values of

are the arithmetic mean values of  .

.

of the linear regression function

of the linear regression function

and

and

is given by:

is given by:

) in the Capital Asset Pricing Model (CAPM). That means that

) in the Capital Asset Pricing Model (CAPM). That means that

… net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

… net income, S … sales, F … fix expenses, V … variable expenses, A … depreciation and amortization, T … taxes, I … interests for debt and X … tax shield we can define net income by:

be the incremental tax rate. We assume that we get full tax shield of

be the incremental tax rate. We assume that we get full tax shield of  . Taxes

. Taxes  are paid on EBIT, that means

are paid on EBIT, that means  .

.  =equity+debt is the asset or enterprise value and d is the debt ratio,

=equity+debt is the asset or enterprise value and d is the debt ratio,  . Substituting that in the previous expression we obtain:

. Substituting that in the previous expression we obtain:

,

,  ,

,  . Variable expenses should have the same correlation to market development as sales, that gives

. Variable expenses should have the same correlation to market development as sales, that gives  . We obtain:

. We obtain:

leads to:

leads to:

with its bilinearity of covariance and get:

with its bilinearity of covariance and get:

as function of

as function of  :

:

.

.

ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that

ist the required return rate of an incremental equity investor. This is the return rate of the completely diversified market portfolio of the appropriate industry segment. The Capital Asset Pricing Model (CAPM) states that  by a given market return rate

by a given market return rate

:

:

,

,  ,

,  ,

,  and

and  . Now we take the parameters of the investment, to which we want to adjusted

. Now we take the parameters of the investment, to which we want to adjusted  . With the

. With the

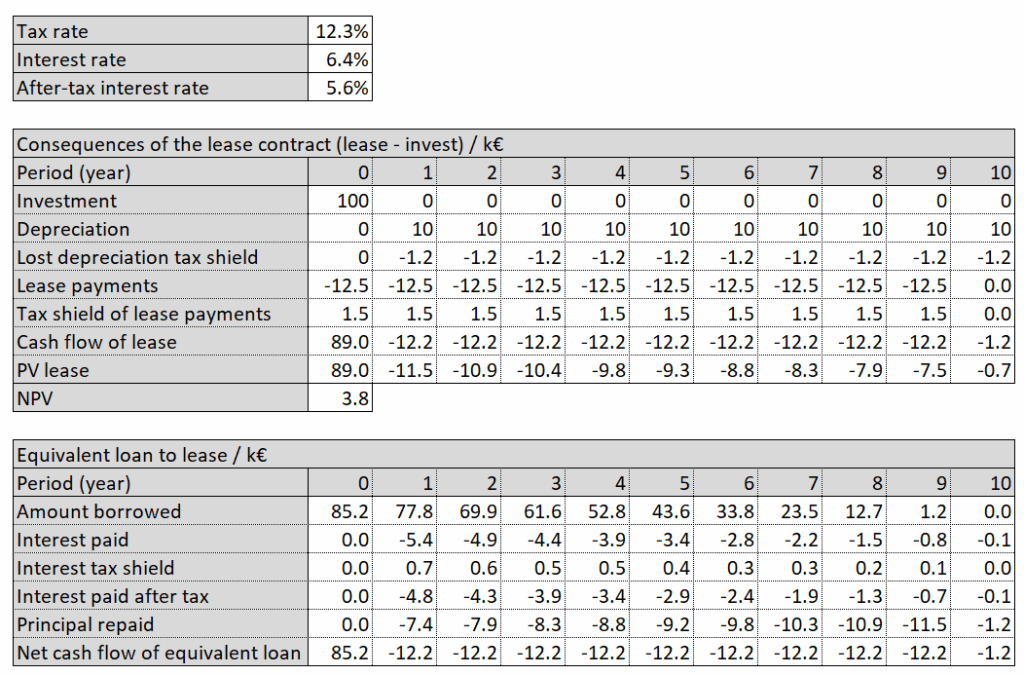

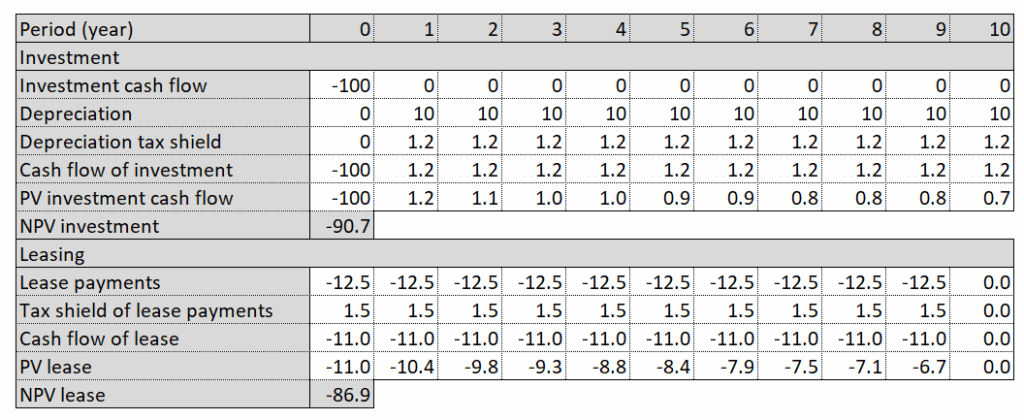

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate

of 100 thousand Euro (k€) or to lease it with annual payments of 12.5 k€. The investment is usable for 10 years and has a no salvage value. The lease payments have to be done in advance and are constant over 10 years. In the table below you can see the consequences of leasing the asset compared to make the investment. Leasing reduces your depreciation, and as a consequence the tax shield because of depreciation is lost. On the other hand the lease payments are fully tax-deductible. We discount the cash flows by the company’s borrowing rate. We can deduct the interest payments from the taxable income. Hence the net cost of borrowing is the after-tax interest rate. So the after-tax interest rate is the effective rate at which a company can transfer debt-equivalent cash flows from one time period to another. With an interest rate  , a tax rate

, a tax rate  we get the net value of lease

we get the net value of lease  :

:![\[V_l=I-\sum_{t=0}^{n}\frac{C_t}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2a7aa6733405981af5a4daba9e405359_l3.png "Rendered by QuickLaTeX.com")

means that leasing is better than doing the investment,

means that leasing is better than doing the investment,  indicates that leasing is worse than investing.

indicates that leasing is worse than investing.

be the investment scenario cash flow and

be the investment scenario cash flow and  be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:

be the lease cash flow in period t. If we discount all cash flows with the same discount rate, the interest rate after taxes in our case, we can separate:![\[\sum_{t=0}^{n}\frac{\left( C_{i,t} - C_{l,t} \right)}{\left( 1+r_d \left(1-r_t \right)\right)^t}=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bbdbe0b0f75b2a0f8bed462292847df8_l3.png "Rendered by QuickLaTeX.com")

![\[=\sum_{t=0}^{n}\frac{ C_{i,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}-\sum_{t=0}^{n}\frac{C_{l,t}}{\left( 1+r_d \left(1-r_t \right)\right)^t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c1d6f85415bf645b3bede9acb1b6f5c1_l3.png "Rendered by QuickLaTeX.com")

is defined by:

is defined by:![\[\beta_p=\frac{cov(r_p,r_m)}{var(r_m)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d4ef4da8f1e8ab77a034e0b8da002c38_l3.png "Rendered by QuickLaTeX.com")

, is the weighted average of its components’ return rates:

, is the weighted average of its components’ return rates:![\[r_p=\sum_{i=1}^{n}\alpha_ir_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7a58dd9b270e96a227c4ced12ba0b223_l3.png "Rendered by QuickLaTeX.com")

![\[cov(r_p, r_m)=cov(\sum_{i=1}^{n}\alpha_ir_i,r_m)=\sum_{i=1}^{n}\alpha_icov(r_p, r_m)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-10de1be8e0635eb826fdc60bf0e5ed6b_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_p=\frac{\sum_{i=1}^{n}\alpha_icov(r_p, r_m)}{var(r_m)}=\sum_{i=1}^{n}\alpha_i\beta_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6678a30fba9b392c30156bc1a214cd77_l3.png "Rendered by QuickLaTeX.com")

.

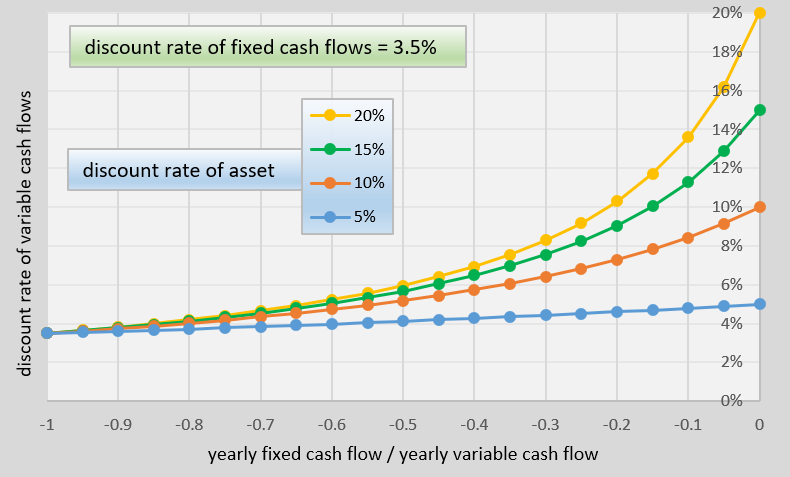

. . Discount rate of fixed cash flows is

. Discount rate of fixed cash flows is  .

. and the yearly fixed cash flow is

and the yearly fixed cash flow is  . Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is

. Both cash flows are estimated to occur at the end of each year, beginning in year 1. The yearly cash flow of the asset is  . Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series.

. Assuming infinite periods we get a perpetuity and can apply the formula of convergent geometric series. is the present value of

is the present value of  discounted with

discounted with  is the present value of

is the present value of  is the present value of

is the present value of  is the present value of

is the present value of  is the present value of

is the present value of ![\[ V_a^a = \frac{C_a}{r_a}, V_f^a=\frac{C_f}{r_a}, V_f^f=\frac{C_f}{r_f},V_v^a=\frac{C_v}{r_a},V_v^v=\frac{C_v}{r_v} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-a5e1ac4bc9c18e87411a96b62844a496_l3.png "Rendered by QuickLaTeX.com")

has to be the same when we discount all cash flows with the asset discount rate

has to be the same when we discount all cash flows with the asset discount rate ![\[ V_a^a=V_v^a+V_f^a=V_f^f+V_v^v \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-3206dc15e5c646023b4aa2e93680a8e8_l3.png "Rendered by QuickLaTeX.com")

![\[ r_v=\frac{r_a}{1-\frac{C_f}{C_v}\left( \frac{r_a}{r_f}-1 \right)} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-95872d0a31aa511d42eef9c28dd1a8bb_l3.png "Rendered by QuickLaTeX.com")

and not on their absolute values.

and not on their absolute values.

the

the  Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same.

Obviously that is true, because asset and variable cash flows and hence also their discount rates are the same. from databases in literature or in the web. In my articles concerning

from databases in literature or in the web. In my articles concerning ![\[\beta^{ind}_{rev}=\beta ^{ind}_{asset} \left( 1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}} \right)^{-1}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cde5ba671ecc1b7b10012fd92a965c0e_l3.png "Rendered by QuickLaTeX.com")

. Hence we obtain:

. Hence we obtain:![\[\beta^{proj}_{rev}=\beta ^{ind}_{asset} \left( 1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}} \right)^{-1}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-353eccdb29a981373f6cdc4bca2ce048_l3.png "Rendered by QuickLaTeX.com")

![\[\beta^{proj}_{asset}=\beta ^{proj}_{rev} \left( 1-\frac{V^{proj}_{fix}}{V^{proj}_{asset}} \right)=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f653639fde45c24bb671287829805624_l3.png "Rendered by QuickLaTeX.com")

![\[= \beta ^{ind}_{asset} \frac{1-\frac{V^{proj}_{fix}}{V^{proj}_{asset}}}{1-\frac{V^{ind}_{fix}}{V^{ind}_{asset}}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2e59a7922907e0e1cf633939c849f6b1_l3.png "Rendered by QuickLaTeX.com")

![\[\beta^{project}_{asset}=1.0 \left( 1+ \frac {1000}{200} \right)=6\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e757d8c2543eaf64339e1fdf4bef1aed_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{P}=\frac{R}{R-C}\beta_{R} - \frac{C}{R-C}\beta_{C}=\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-214f6b4aa833f50c0348169b35112362_l3.png "Rendered by QuickLaTeX.com")

![\[=\frac{1200}{1200-1000}1 - \frac{1000}{1200-1000}0=6\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-58210695bcd89b8fbc6f9c8b560ad8fa_l3.png "Rendered by QuickLaTeX.com")

, variable costs

, variable costs  and revenues

and revenues  cannot be found easily. But we can try to approximate them with P&L or balance sheet figures, which are available more eaysily. Let us consider eternal yearly revenues

cannot be found easily. But we can try to approximate them with P&L or balance sheet figures, which are available more eaysily. Let us consider eternal yearly revenues  , yearly fixed costs

, yearly fixed costs  and yearly variable costs

and yearly variable costs  . The risk free rate is

. The risk free rate is ![\[\beta _{asset} = \beta_{rev} \left( 1 - \frac{V_{fix}}{V_{asset}} \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1dfd5750e036dfe0ed0c2580165d58d1_l3.png "Rendered by QuickLaTeX.com")

![\[V_{fix}=- \frac{\alpha R}{r_f}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8c2173bb867d2039c7c24b01280886db_l3.png "Rendered by QuickLaTeX.com")

![\[V_{asset}= \frac{R - \alpha R - \beta R}{r_m}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2047a4c2ba3b0169ee09b36933d3035a_l3.png "Rendered by QuickLaTeX.com")

:

:![\[\beta _{asset} = \beta_{rev} \left( 1 + \frac{\frac{\alpha R}{r_f}}{\frac{R - \alpha R - \beta R}{r_m}} \right) = \beta_{rev} \left( 1 + \frac{r_m}{r_f}\frac{\alpha}{1-\alpha-\beta} \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2d2c815f15ff7b3feca76b5a7bb8316c_l3.png "Rendered by QuickLaTeX.com")

and

and  approximately, so

approximately, so  ,

,  is the ratio of annual fixed costs to annual profit. That means that you have to multiply that factor with the 2, when applying P&L figures in approximation and not present values.

is the ratio of annual fixed costs to annual profit. That means that you have to multiply that factor with the 2, when applying P&L figures in approximation and not present values.  for the buying and

for the buying and  for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.

for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.![\[NPV_b=\sum_{i}^{}\gamma_{b,i}C_{b,i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7edf54aa8061c21fae0649b7cb42febf_l3.png "Rendered by QuickLaTeX.com")

![\[NPV_l=\sum_{j}^{}\gamma_{l,j}C_{l,j}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2ff141704520007119cf9e00400279cc_l3.png "Rendered by QuickLaTeX.com")

.

. ,

,  , which is the sum of different assets values

, which is the sum of different assets values  :

:![\[C(t)=\sum_{i}^{}C_i(t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-238c5682b36c90200f3872ee0001a260_l3.png "Rendered by QuickLaTeX.com")

the asset values are

the asset values are  and

and  with

with  . The asset value

. The asset value  is developing in time

is developing in time  , that means:

, that means:![\[C_i (t)=C_i(0)exp(r_i t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-199dec8af5bafc55f69c19ffd13b2d2b_l3.png "Rendered by QuickLaTeX.com")

, that describes the development of the aggregated asset value

, that describes the development of the aggregated asset value  . Setting

. Setting  we obtain:

we obtain:![\[r=\frac{1}{t}ln\frac{C(t)}{C(0)}=\frac{1}{t}ln\left( \sum_{i}^{} \left \frac{C_i(0)}{C(0)} exp \left( r_i t \right) \right \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fb659cb84b82fa3fac2f0009b503dd4b_l3.png "Rendered by QuickLaTeX.com")

and

and  . Hence we get a first order approximation of

. Hence we get a first order approximation of ![\[r\simeq \frac{1}{t}\left( \sum_{i}^{} \left( \frac{C_i(0)}{C(0)} \left( 1+ r_i t \right) \right) -1 \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-87db3d07482630425a989b6495027b30_l3.png "Rendered by QuickLaTeX.com")

![\[r\simeq \sum_{i}^{} \frac{C_i(0)}{C(0)} r_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5806f016a86a9e819753e1a5e6579448_l3.png "Rendered by QuickLaTeX.com")

return rate

return rate ![\[WACC=r=\frac{D}{E+D}r_D+\frac{E}{E+D}r_E\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7b9fcbf01c1f74e6a122461f37027337_l3.png "Rendered by QuickLaTeX.com")

or

or  . With a substitution of

. With a substitution of  , you can transform these two return rates into each other.

, you can transform these two return rates into each other. , is the sum of revenues’ value,

, is the sum of revenues’ value, ![\[V_{asset}=V_{rev}+V_{var}+V_{fix}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cf23103bfba3ed586bd4ee1464a7b4d8_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{asset}=\frac{\beta_{rev} V_{rev} + \beta_{var} V_{var}+ \beta_{fix} V_{fix}}{V_{asset}}.\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f9abbfbe3a34248c1ea171096730d969_l3.png "Rendered by QuickLaTeX.com")

and therefore

and therefore  . We obtain:

. We obtain:![\[\beta_{asset}=\frac{V_{rev}\beta_{rev} + V_{var}\beta_{var}}{V_{asset}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c8bd7662c544e7ee1cc1dfd493bc7da0_l3.png "Rendered by QuickLaTeX.com")

. We get:

. We get:![\[\beta_{asset}=\beta_{rev} \frac{V_{rev} + V_{var}}{V_{asset}}=\beta_{rev} \left( 1-\frac{V_{fix}}{V_{asset}} \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-460385135a1bed426f4e8cc7f7cb9662_l3.png "Rendered by QuickLaTeX.com")

, and the value of the asset is positive,

, and the value of the asset is positive,  , in ordinary cases. The expression in the bracket becomes

, in ordinary cases. The expression in the bracket becomes  . That means that the beta of the asset is higher than the beta of the revenues,

. That means that the beta of the asset is higher than the beta of the revenues,  . Obviously that is true, because adding fixed costs increases the beta of the asset. This effect is known as operating leverage.

. Obviously that is true, because adding fixed costs increases the beta of the asset. This effect is known as operating leverage. and

and  .

. ![\[r_E=r_f+\beta _{rev}\left( r_m - r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-333b7bf948d2e673718fe660bee9b387_l3.png "Rendered by QuickLaTeX.com")

considering debt

considering debt ![\[r_{rev}=\frac{D}{E+D} \left( 1-t \right) r_D + \frac{E}{E+D} r_E\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8816ce85e3ebb914b2b3b891bb1d463d_l3.png "Rendered by QuickLaTeX.com")

, divided by the present value of all investment cash flows,

, divided by the present value of all investment cash flows,  . Hereby it is important how we define the term investment. You can have a look at my proposal in this

. Hereby it is important how we define the term investment. You can have a look at my proposal in this ![\[PI=\frac{PV_C}{PV_I}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f8912a2a1acef3578476fece21ce73f7_l3.png "Rendered by QuickLaTeX.com")

shows how much value is created per investment. All projects with a

shows how much value is created per investment. All projects with a  are creating additional value to the investors, all projects with a

are creating additional value to the investors, all projects with a  are destroying value.

are destroying value.![\[PI^*=\frac{PV_C-PV_I}{PV_I}=\frac{PV_C}{PV_I}-1=PI-1\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-852d8bdcfe0d8e08d8e4e08ea95efc33_l3.png "Rendered by QuickLaTeX.com")

:

:![\[PIA=\frac{PI}{A_{n,r}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-cae3fb545351871cad5018e3c01b814b_l3.png "Rendered by QuickLaTeX.com")

![\[A_{n,r}=\frac{1}{r}\left( 1-\frac{1}{\left( 1+r \right)^n} \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bb804176bdcf6a6e5abb0a6b97de6a61_l3.png "Rendered by QuickLaTeX.com")

![\[I_t^{res}:=f_t+c_t-c_{t-1}-c_{t-1}i_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bc65d4df301a3c2e176603cf8e26139f_l3.png "Rendered by QuickLaTeX.com")

is the cash flow in period

is the cash flow in period  the fixed capital in period

the fixed capital in period  the discount rate in period

the discount rate in period  is just the depreciation in period

is just the depreciation in period ![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}(1+i_t)-c_t)\rho_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-69a2df2c6eec9bcf4204b280e7e4d618_l3.png "Rendered by QuickLaTeX.com")

is the discount factor in period

is the discount factor in period  . That means

. That means  . With that we obtain:

. With that we obtain:![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}\rho_{t-1} - c_t \rho_t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-80f028ea0a1e5aa789c7c681959a662b_l3.png "Rendered by QuickLaTeX.com")

. And if all fixed asset is depreciated in the considered n periods, we can set

. And if all fixed asset is depreciated in the considered n periods, we can set  . With these two premises we realize that all terms of the sum become zero.

. With these two premises we realize that all terms of the sum become zero.![\[\sum_{t=0}^{n}(f_t-I_t^{res}) \rho_t = c_{-1} \rho_{-1} - c_n \rho_n=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-97221d236f91df1aa277ca8486b5c86b_l3.png "Rendered by QuickLaTeX.com")

. The discount factors

. The discount factors  can be different for each cach flow

can be different for each cach flow ![\[NPV=\sum_{i}^{}\gamma _i c_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-be714489173707f0b2e1b021beec0ef7_l3.png "Rendered by QuickLaTeX.com")

(uniformity). Let

(uniformity). Let ![\[NPV=\sum_{t}^{}\gamma _t C_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-34fe10e182bb18789975d41fbebb21cb_l3.png "Rendered by QuickLaTeX.com")

has polynomial character in

has polynomial character in ![\[NPV=\sum_{t}^{}C_t\gamma ^t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6e05f66d719263443df328c80a352a1f_l3.png "Rendered by QuickLaTeX.com")

we get the well-known formula:

we get the well-known formula:![\[NPV=\sum_{t}^{}C_t\left( 1+i \right) ^{-t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f21d29c636ae7845b1eb805b47a261df_l3.png "Rendered by QuickLaTeX.com")

is now defined to be the values of

is now defined to be the values of ![\[NPV=\sum_{t}^{}C_t\left( 1+i^{IRR} \right) ^{-t}=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-058630d81fc54ddadec91380bef860e6_l3.png "Rendered by QuickLaTeX.com")

are calculated by adding risk premiums to the risk-free rate. Considering the Capital Asset Pricing Model (CAPM) the expected value of the equity return rate is:

are calculated by adding risk premiums to the risk-free rate. Considering the Capital Asset Pricing Model (CAPM) the expected value of the equity return rate is:![\[E \left( r_e \right)= r_f+\beta \left( E\left( r_m \right) - r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-38e62fabc01a82f5db7e3983991acc6e_l3.png "Rendered by QuickLaTeX.com")

of the valuation. But be aware that this is an approximation and can be false in some cases.

of the valuation. But be aware that this is an approximation and can be false in some cases. having annual return rates

having annual return rates  and standard deviations of the annual return rates

and standard deviations of the annual return rates  . The variance of the portfolio return rate is given by:

. The variance of the portfolio return rate is given by:![\[var\left( R_P \right)=\sum_{i}^{}x_i\text{cov}\left( R_i, R_P \right) \text{, or}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-213e53714645a6928f8809c075b35994_l3.png "Rendered by QuickLaTeX.com")

![\[ var\left( R_P \right) =\sum_{i}^{}x_i\sigma\left( R_i \right)\sigma\left( R_P \right)\text{corr}\left( R_i, R_P \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-89d31827c4e75a2404edbcb4707fbdcc_l3.png "Rendered by QuickLaTeX.com")

gives the standard deviation

gives the standard deviation ![\[\sigma\left( R_P \right)=\sum_{i}^{}x_i\sigma\left( R_i \right)\text{corr}\left( R_i, R_P \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-db9c91da9142d49d0592f3f742409da5_l3.png "Rendered by QuickLaTeX.com")

.

.![\[\frac{E\left( R_P\right)-r_f}{\sigma \left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-45e12ba3a38d9bebc05f90ab64f78c59_l3.png "Rendered by QuickLaTeX.com")

is the expected value of

is the expected value of  and

and ![\[\text{E}\left( R_i \right)-r_f > \sigma\left( R_i \right)\text{corr}\left( R_i,R_P \right)\frac{E\left( R_P\right)-r_f}{\sigma\left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-90f6b90208a26c8b429370ea22e0168b_l3.png "Rendered by QuickLaTeX.com")

of the new investment to the existing portfolio:

of the new investment to the existing portfolio:![\[\beta_i^P=\frac{\sigma\left( R_i \right)\text{corr}\left( R_i,R_P \right)}{\sigma\left( R_P \right)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-604cc66ff63230e502c823c1520bc1b2_l3.png "Rendered by QuickLaTeX.com")

![\[\text{E}\left( R_i \right) > r_f+\beta_i^P\left( E\left( R_P\right)-r_f \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-750ab8b8d312bc0ee256f6103ec6e4fb_l3.png "Rendered by QuickLaTeX.com")

![\[ r_i = r_f+\beta_i^P\left( E\left( R_P\right)-r_f \right) \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fc1f59b1f6bff846398674e4242b6bbb_l3.png "Rendered by QuickLaTeX.com")

. The sign of NPV indicates whether an asset generates value to the fund providers (debt and equity) or not. If only the amount, but not the sign of NPV changes by a time shift, the decision to allocate the project or not does not change. That means that the decision itself does not depend on the time scale. In many books I have read that argument. But is this really true?

. The sign of NPV indicates whether an asset generates value to the fund providers (debt and equity) or not. If only the amount, but not the sign of NPV changes by a time shift, the decision to allocate the project or not does not change. That means that the decision itself does not depend on the time scale. In many books I have read that argument. But is this really true? we can write

we can write  instead of

instead of  . The NPV of the project at the “present” time

. The NPV of the project at the “present” time  , is:

, is:![\[NPV_0=\sum_{i}^{}E(C_i) e^{-\alpha t_i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-210d871123a0c687f1a41a644f034588_l3.png "Rendered by QuickLaTeX.com")

is the expected value of the i-th cash flow component. When we shift time by

is the expected value of the i-th cash flow component. When we shift time by  :

:![\[NPV_ {\Delta t} =\sum_{i}^{}E(C_i) e^{-\alpha (t_i+ {\Delta t} )}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-9004eb4b37f2bef2f6809e94c349a420_l3.png "Rendered by QuickLaTeX.com")

![\[ NPV_ {\Delta t} = e^{ -\alpha \Delta t} \sum_{i}^{}E(C_i) e^{-\alpha (t_i )}= e^{ -\alpha \Delta t} NPV_0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-03541590c7a5b90db51ed95302ab6383_l3.png "Rendered by QuickLaTeX.com")

, the sign of

, the sign of  respectively, for cash flow

respectively, for cash flow ![\[NPV_0=\sum_{i}^{}E(C_i) e^{-\alpha_i t_i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-19b1f47cb1ceb032a87c531f81c1d140_l3.png "Rendered by QuickLaTeX.com")

![\[NPV_ {\Delta t} =\sum_{i}^{}E(C_i) e^{-\alpha_i (t_i+ {\Delta t} )}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1378ee94d492c34b8db2e3d644f37a21_l3.png "Rendered by QuickLaTeX.com")

![\[WACC=\frac{D}{D+E}r_{D}\left( 1-t \right)+\frac{E}{D+E}r_{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-c150dac17c089c73e6b19670b795c77d_l3.png "Rendered by QuickLaTeX.com")

” that comes from tax shield savings.

” that comes from tax shield savings.  and ending at time

and ending at time  . In

. In  and an absolute tax shield value of

and an absolute tax shield value of  .

.  that allows us to discount the cash flow excluding tax shield but including the tax shield effect in the present value in

that allows us to discount the cash flow excluding tax shield but including the tax shield effect in the present value in ![\[\frac{C_1+T_1}{1+r}=\frac{C_1}{1+r^{*}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0458f1a13c8435c88c2b5535cb475186_l3.png "Rendered by QuickLaTeX.com")

and

and ![\[r^{*}=\frac{C_1r-T_1}{C_1+T_1}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6d83f7108bf6d4e8988e90a3cdf1cceb_l3.png "Rendered by QuickLaTeX.com")

and equity

and equity  . The discounted value of the cash flows must be the sum of debt and equity. With

. The discounted value of the cash flows must be the sum of debt and equity. With  we obtain:

we obtain:![\[r^*=r-\frac{T_1}{D_0+E_0}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1c8bb7f3255a36b45261bec3c7096fea_l3.png "Rendered by QuickLaTeX.com")

![\[r^*=\frac{D_0}{D_0+E_0}r_{D}+\frac{E_0}{D_0+E_0}r_{E} -\frac{T_1}{D_0+E_0} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7c8e7987fcf2f55ab5b36debc557b774_l3.png "Rendered by QuickLaTeX.com")

. Hence we get the well known expression for

. Hence we get the well known expression for ![\[r^*=\frac{D_0}{D_0+E_0}r_{D}\left( 1-t \right)+\frac{E_0}{D_0+E_0}r_{E}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fb913c6d8a6c7d49e7952f3998c0a6b0_l3.png "Rendered by QuickLaTeX.com")

, maybe a maximum share of EBITDA in

, maybe a maximum share of EBITDA in ![\[r^*=\frac{D_0}{D_0+E_0}r_{D}+\frac{E_0}{D_0+E_0}r_{E} -\frac{ \min \left( D_0 r_D t , T_1^{\text{max}} \right)}{D_0+E_0} \]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-4c26608e35c0cc7701004b1985686860_l3.png "Rendered by QuickLaTeX.com")