Joachim Kuczynski, 27 November 2024

Die Bewertung von Investitionen und Projekten (bzw. allgemein Assets) basiert auf der Verschiebung und Anpassung von Cash Flows auf der Zeitachse. Geht diese Verschiebung rückwärts in der Zeit, so spricht man von Diskontierung. Eine Verschiebung vorwärts auf der Zeitachse nennt man Kapitalisierung. Viele Analysten verwenden für Diskontierung und Kapitalisierung in einem Projekt dieselbe Rate. Doch darf man die Cash Flows mit demselben Rate tatsächlich auf der Zeitachse vor und zurück schieben? Die Antwort darauf ist ein klares Nein.

Die Diskontierungsrate eines Cash Flows basiert auf seinem ihm innewohnenden Risiko (Volatilität). Im allgemeinen ist sie unabhängig von den Risikopräferenzen der Kapitalgeber, sofern dessen Anlagenportfolio ausreichend diversifierziert ist. Die Kapitalisierungsrate eines Cash Flows basiert hingegen auf den Risikopräferenzen und der Portfoliodiversifizierung des Unternehmens bzw. dessen Kapitalgeber. Die Kapitalisierungrate ist unabhängig davon, welches Risiko dem initialen Cash Flow innewohnte. Wenn er einmal zur Kapitalisierung zur Verfügung steht, spielt es keine Rolle, unter welchen Umständen er zustandekam. Diskontierungsrate und Kapitalisierungsrate sind prinzipiell ganz unterscheidlicher Natur. Sie in Kalkulationen gleichzusetzen ist grundlegender, logischer Fehler.

Es gibt Kennzahlen der Investitionsbewertung, die eine Rekapitalisierung rückfliessender Cash Flows beinhalten. Ein bekanntes Beispiel ist der Modifizierte Interne Zinssatz bzw. der Baldwin-Zins. Dort wird üblicherweise angenommen, dass Diskontierung als auch Wiederveranlagung mit dem WACC erfolgen. Der WACC basiert auf der Renditeerwartung der Kapitalgeber. Diese müssen sich aber keineswegs mit den Renditemöglichkeiten des investierenden Unternehmens decken. Oft werden zur Diskontierung zudem zusätzliche Raten („risk premium“) addiert. Damit möchte man beispielsweise Währungs- oder Standortrisiken berücksichtigen. Nimmt man nun dieselbe Rate auch für die Kapitalisierung, unterstellt man eine erhöhte Wiederveranlagungsrate für das Unternehmen. Dies ist natürlich falsch und erhöht den Fehlerhaftigkeit der Kalkulation weiter.

Zusammenfassend kann man festhalten, dass eine Gleichstellung von Diskontierungsrate und Kapitalisierungsrate grundlegend falsch ist. Viele Formeln lass sich mit einer Gleichsetzung zwar bequem vereinfachen. Die Ergebnisse der Kalkulation sind aber damit nicht mehr valide. Richtige und aussagefähige Ergebnisse der Investitionsrechnung sind jedoch die Grundlage für richtigen Investitionsentscheidungen.

![\[\beta_{revenue}=\beta_{\text{fixed exp.}}\frac{\text{PV(fixed exp.)}}{\text{PV(revenue)}}+\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-22ca865e4c21271c0f3bc44dca490e27_l3.png "Rendered by QuickLaTeX.com")

![\[+\beta_{\text{var. exp.}}\frac{\text{PV(var. exp.)}}{\text{PV(revenue)}}+\beta_{\text{asset}}\frac{\text{PV(asset)}}{\text{PV(revenue)}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8f482de4ea88b0dd2d4748447a6138c0_l3.png "Rendered by QuickLaTeX.com")

. The betas of revenues and variable expenses are more or less the same, because they are both related to the output. Therefore we can substitute

. The betas of revenues and variable expenses are more or less the same, because they are both related to the output. Therefore we can substitute  for

for  .

. ![\[\beta_{\text{asset}}=\beta_{\text{revenue}}\frac{\text{PV(revenue)-PV(var.exp.)}}{\text{PV(asset)}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-06005d4a557072f737deb59a43c355e4_l3.png "Rendered by QuickLaTeX.com")

![\[\beta_{\text{asset}}=\beta_{\text{revenue}}\left[ 1 + \frac{\text{PV(fixed exp.)}}{\text{PV(asset)}}\right]\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-209d0fc4f949491090ced1b6de4e5504_l3.png "Rendered by QuickLaTeX.com")

![\[\text{DOL}= 1 + \frac{\text{fixed exp.}}{\text{profits}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5d31b885a5ed690021f7a54b33716f05_l3.png "Rendered by QuickLaTeX.com")

is the average asset beta of the industry segment, which has an average ratio of fixed expenses to profits.

is the average asset beta of the industry segment, which has an average ratio of fixed expenses to profits.  . The discount factors

. The discount factors  can be different for each cach flow

can be different for each cach flow ![\[NPV=\sum_{i}^{}\gamma _i c_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-be714489173707f0b2e1b021beec0ef7_l3.png "Rendered by QuickLaTeX.com")

, because all cash flows one period

, because all cash flows one period  (uniformity). Let

(uniformity). Let  be the sum of the cash flows in period

be the sum of the cash flows in period ![\[NPV=\sum_{t}^{}\gamma _t C_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-34fe10e182bb18789975d41fbebb21cb_l3.png "Rendered by QuickLaTeX.com")

has polynomial character in

has polynomial character in ![\[NPV=\sum_{t}^{}C_t\gamma ^t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-6e05f66d719263443df328c80a352a1f_l3.png "Rendered by QuickLaTeX.com")

be the annual interest rate to discount cash flows. Setting

be the annual interest rate to discount cash flows. Setting  we get the well-known formula:

we get the well-known formula:![\[NPV=\sum_{t}^{}C_t\left( 1+i \right) ^{-t}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f21d29c636ae7845b1eb805b47a261df_l3.png "Rendered by QuickLaTeX.com")

is now defined to be the values of

is now defined to be the values of ![\[NPV=\sum_{t}^{}C_t\left( 1+i^{IRR} \right) ^{-t}=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-058630d81fc54ddadec91380bef860e6_l3.png "Rendered by QuickLaTeX.com")

can have

can have

![\[MIRR=\sqrt[n]{\frac{\text{FV(contribution cash flows,WACC)}}{\text{PV(invest cash flows, financing rate)}}}-1\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bc3151b9811774776aaad69dd41965ad_l3.png "Rendered by QuickLaTeX.com")

, the Baldwin rate can decrease. This is because the number of periods increases and the value of the root decreases. Cases that lead to wrong results are not acceptable for decision key figure.

, the Baldwin rate can decrease. This is because the number of periods increases and the value of the root decreases. Cases that lead to wrong results are not acceptable for decision key figure. … before-tax discount rate

… before-tax discount rate … after-tax discount rate

… after-tax discount rate … rate of debt to sum of equity

… rate of debt to sum of equity  and debt

and debt  ,

,

… debt interest rate

… debt interest rate … equity interest rate

… equity interest rate![\[r=\left( 1-L \right)r_{E}+Lr_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e27f6e854c47d27bb1651ad6e45e2bde_l3.png "Rendered by QuickLaTeX.com")

we have:

we have:![\[r_{E}=\frac{r-Lr_D}{1-L}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-8cdf8fee024408f1a475932c0da21d94_l3.png "Rendered by QuickLaTeX.com")

![\[r^{*}=\left( 1-L \right)r_{E}+L\left( 1-t \right)r_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-f19765a904cf1b8b48832af962b2c107_l3.png "Rendered by QuickLaTeX.com")

![\[r^{*}= r -Ltr_D\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-95ee3f0f11e1c330099229798f192ac0_l3.png "Rendered by QuickLaTeX.com")

, which is the sum of different assets values

, which is the sum of different assets values  :

:![\[C(t)=\sum_{i}^{}C_i(t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-238c5682b36c90200f3872ee0001a260_l3.png "Rendered by QuickLaTeX.com")

the asset values are

the asset values are  and

and  with

with  . The asset value

. The asset value  is developing in time

is developing in time  , that means:

, that means:![\[C_i (t)=C_i(0)exp(r_i t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-199dec8af5bafc55f69c19ffd13b2d2b_l3.png "Rendered by QuickLaTeX.com")

. Setting

. Setting  we obtain:

we obtain:![\[r=\frac{1}{t}ln\frac{C(t)}{C(0)}=\frac{1}{t}ln\left( \sum_{i}^{} \left \frac{C_i(0)}{C(0)} exp \left( r_i t \right) \right \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-fb659cb84b82fa3fac2f0009b503dd4b_l3.png "Rendered by QuickLaTeX.com")

and

and  . Hence we get a first order approximation of

. Hence we get a first order approximation of ![\[r\simeq \frac{1}{t}\left( \sum_{i}^{} \left( \frac{C_i(0)}{C(0)} \left( 1+ r_i t \right) \right) -1 \right)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-87db3d07482630425a989b6495027b30_l3.png "Rendered by QuickLaTeX.com")

![\[r\simeq \sum_{i}^{} \frac{C_i(0)}{C(0)} r_i\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5806f016a86a9e819753e1a5e6579448_l3.png "Rendered by QuickLaTeX.com")

![\[WACC=r=\frac{D}{E+D}r_D+\frac{E}{E+D}r_E\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7b9fcbf01c1f74e6a122461f37027337_l3.png "Rendered by QuickLaTeX.com")

or

or  . With a substitution of

. With a substitution of  , you can transform these two return rates into each other.

, you can transform these two return rates into each other.![\[I_t^{res}:=f_t+c_t-c_{t-1}-c_{t-1}i_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-bc65d4df301a3c2e176603cf8e26139f_l3.png "Rendered by QuickLaTeX.com")

is the cash flow in period

is the cash flow in period  the fixed capital in period

the fixed capital in period  the discount rate in period

the discount rate in period  is just the depreciation in period

is just the depreciation in period ![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}(1+i_t)-c_t)\rho_t\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-69a2df2c6eec9bcf4204b280e7e4d618_l3.png "Rendered by QuickLaTeX.com")

is the discount factor in period

is the discount factor in period  . That means

. That means  . With that we obtain:

. With that we obtain:![\[\sum_{t=0}^{n}(f_t-I_t^{res})\rho_t=\sum_{t=0}^{n}(c_{t-1}\rho_{t-1} - c_t \rho_t)\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-80f028ea0a1e5aa789c7c681959a662b_l3.png "Rendered by QuickLaTeX.com")

. And if all fixed asset is depreciated in the considered n periods, we can set

. And if all fixed asset is depreciated in the considered n periods, we can set  . With these two premises we realize that all terms of the sum become zero.

. With these two premises we realize that all terms of the sum become zero.![\[\sum_{t=0}^{n}(f_t-I_t^{res}) \rho_t = c_{-1} \rho_{-1} - c_n \rho_n=0\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-97221d236f91df1aa277ca8486b5c86b_l3.png "Rendered by QuickLaTeX.com")

for the buying and

for the buying and  for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.

for the leasing scenario). Adding up all present values you get a net present value (NPV) of the buying case and a NPV of the leasing case.![\[NPV_b=\sum_{i}^{}\gamma_{b,i}C_{b,i}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-7edf54aa8061c21fae0649b7cb42febf_l3.png "Rendered by QuickLaTeX.com")

![\[NPV_l=\sum_{j}^{}\gamma_{l,j}C_{l,j}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-2ff141704520007119cf9e00400279cc_l3.png "Rendered by QuickLaTeX.com")

.

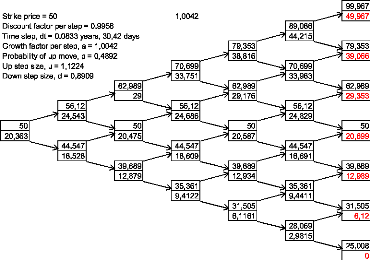

. zum Zeitpunkt

zum Zeitpunkt ![\[C_0=\frac{\alpha C_{u,t_1}+(1-\alpha )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d245e3e501c03334a52b0327fc44aea3_l3.png "Rendered by QuickLaTeX.com")

and

and  sind die Optionswerte der up und down Entwicklungen zum Zeitpunkt

sind die Optionswerte der up und down Entwicklungen zum Zeitpunkt  .

.  und

und  ist hierin die risikoneutrale Wahrscheinlichkeit der up Bewegung in

ist hierin die risikoneutrale Wahrscheinlichkeit der up Bewegung in  ist die risikoneutrale Wahrscheinlichkeit der down Bewegung in

ist die risikoneutrale Wahrscheinlichkeit der down Bewegung in ![\[\alpha=\frac{(1+r)^T-d}{u-d}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-53e84d5ecdafd962f48030489a62864d_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{\frac{(1+r)^T-d}{u-d} C_{u,t_1}+(1-\frac{(1+r)^T-d}{u-d} )C_{d,t_1}}{(1+r)^T }\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-4585ecf3307b3ea36a992a134bd156a8_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{( (1+r)^T-d ) C_{u,t_1}+(u-(1+r)^T )C_{d,t_1}}{(1+r)^T (u-d)}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-e41bd7434143afaf1fc36677db98383c_l3.png "Rendered by QuickLaTeX.com")

und

und  sind definiert als die Verhältnisse von up und down Entwicklung zum Erwartungswert des Zustands in

sind definiert als die Verhältnisse von up und down Entwicklung zum Erwartungswert des Zustands in  :

:![\[u= \frac{EV(S_{t_0})}{S_{u,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-d9deab9057d9c6d1f3a1ba8f0e6ce779_l3.png "Rendered by QuickLaTeX.com")

![\[d= \frac{EV(S_{t_0})}{S_{d,t_1}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-875c14eb30bf1a7d78b5173c9c6dfadf_l3.png "Rendered by QuickLaTeX.com")

und Zustand down

und Zustand down  nicht vorgekommen. Vielfach wird nun argumentiert, dass die Wahrscheinlichkeiten der beiden Realzustände den Optionswert nicht beeinflussen. Dies stimmt nicht. Der Erwartungwert von Zustand

nicht vorgekommen. Vielfach wird nun argumentiert, dass die Wahrscheinlichkeiten der beiden Realzustände den Optionswert nicht beeinflussen. Dies stimmt nicht. Der Erwartungwert von Zustand  und damit von

und damit von  hängen von diesen Wahrscheinlichkeiten ab. Der Erwartungswert des Zustands in

hängen von diesen Wahrscheinlichkeiten ab. Der Erwartungswert des Zustands in ![\[EV(S_{t_0})=\frac{EV(S_{t_1})}{(1+D)^T}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{(1+D)^T}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-1bde57d477d9f69bdf954feb24df97ba_l3.png "Rendered by QuickLaTeX.com")

![\[u=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{u,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-ba3a6fc511e4ae945efcc80c544226d2_l3.png "Rendered by QuickLaTeX.com")

![\[d=\frac{EV(S_{t_0})}{S_{u,t_1}}=\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-df6488617bbde3eaabec1cf22b39708f_l3.png "Rendered by QuickLaTeX.com")

![\[C_0=\frac{( (1+r)^T-\frac{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}{S_{d,t_1}(1+D)^{T}}) C_{u,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}+\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-0769b16c961ea4a991747ee6dec7ad23_l3.png "Rendered by QuickLaTeX.com")

![\[+\frac{(\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-(1+r)^T )C_{d,t_1}}{(1+r)^T ( \frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{u,t_1}(1+D)^{T}}}-\frac{{pS_{u,{t_1}}+(1-p)S_{d,{t_1}}}}{{S_{d,t_1}(1+D)^{T}}})}\]](https://www.financeinvest.at/wp-content/ql-cache/quicklatex.com-5b78a3049855170fe758d7f83b5e5355_l3.png "Rendered by QuickLaTeX.com")

und

und  der realen up

der realen up  und down Zustände

und down Zustände  abhängt. Das wollten wir zeigen. q.e.d.

abhängt. Das wollten wir zeigen. q.e.d.